Politics is heating up for the summer, but there were at least a few more reasons to hope that underlying inflation pressures may be starting to cool.

This is the second weekly wrap of the key points from my social media posts on the UK economy, on the markets, and occasionally on the politics too.

Bank Holiday weekend (Saturday 23 May to Monday 25 May)

The UK markets were closed and there was no new economic data, but the politicians kept busy.

Reform dominated the headlines with a proposal that people who earn less than £75,000 and work overtime above a 40-hour week would pay no income tax on the extra hours. However, this idea was roundly criticised by economists (including myself in an earlier post) and by tax specialists (notably in this briefing by Dan Neidle).

In short, I argued that Reform’s proposal was well-intentioned but still unfair, complex, and distortionary. There are also better ways to make work pay.

Dan Neidle’s briefing also included a sensible list of alternative tax cuts, all providing a bigger bang for the buck, Interestingly, the list was topped by the abolition of stamp duty on shares, which would be harder to sell to the voters but also much better economics! This is explained further in this CPS note referencing analysis by Oxera.

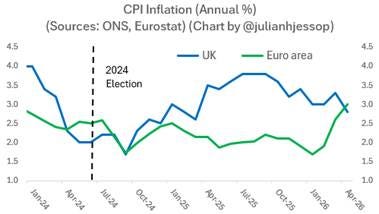

In the interests of “balance” I also had another pop at Rachel Reeves, who claimed last week that “We promised to cut inflation – and we have”.

In reality, Labour inherited an on-target inflation rate of 2%, then saddled businesses with a load of extra costs, lifting the CPI measure to 3.8% last autumn. Inflation has since fallen back, but it was still 2.8% in April.

What’s more, essentially all that Labour has done to help is transfer some charges from household bills to general taxation, or more borrowing, which is hardly “fixing the foundations”.

Tuesday 26 May

Tuesday brought some slightly better news on inflation. Two separate surveys for May, from the BRC and from the CBI, suggested that shop price inflation is still being held down by weak demand and strong competition, despite rising costs. It is tempting to add that rather than lecturing retailers and demonising supermarkets, the government could do its bit by keeping costs down too.

Meanwhile, the Guardian ran an “exclusive” headlined “Rachel Reeves tells ministers to ‘buy British’ in four key industries”, targeting the procurement of ships, steel, energy and AI. It was depressing to see the Treasury telling Ministers to “buy British” regardless of cost, rather than prioritise the interests of taxpayers and users of public services.

It was also odd to see a government which says it wants closer alignment with the EU apparently willing to trample all over EU (and WTO?) procurement rules. Presumably there is some sort of “national security” exemption, but this feels like desperate stuff.

Wednesday 27 May

Ofgem confirmed that the energy price cap will rise by 13% from July. This was at least broadly in line with expectations, while the risks of the second-round effects that might prompt the Bank of England to respond by raising interest rates are fading quickly.

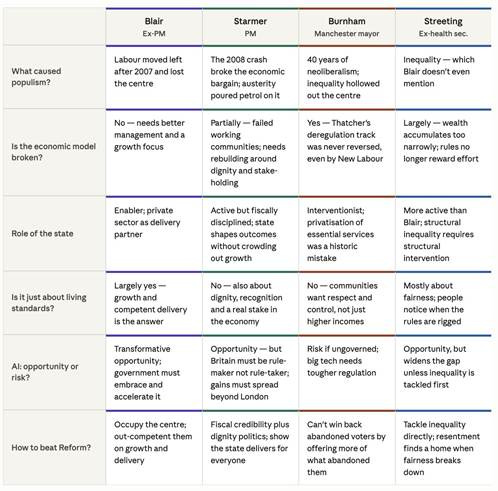

Another big talking point was the continuing fallout from Tony Blair’s essay on the state of the UK economy – the first of several from Labour figures and arguably the best received more widely. I would just add that even Tony Blair now seems sceptical about realigning with (let alone rejoining) an unreformed European Union.

He had some positive things to say about Europe too, of course. But he flagged up the problem that the UK is choosing to negotiate from a position of weakness, and that the EU’s bias towards over-regulation could be a particular threat to the tech sector.

One more EU story. The Guardian reported that the “EU could deny new member states veto rights as bloc pushes for enlargement”. This restriction would be another huge hurdle to rejoin if it also applied to the UK.

The intention is that this particular restriction would only apply to smaller, poorer new entrants, and that it would only be temporary (there are not supposed to be two tiers of EU membership). But these countries might be rightly annoyed if the UK could just waltz back in on the same terms it had before, whereas they would have fewer rights.

Some officials from existing members (and polls of citizens) are already suggesting that the UK cannot keep its previous opt-outs, or the budget rebate.

Moreover, this proposal reflects the general direction of travel for the EU, which is to towards “ever closer union”, with more power centralised in institutions like the European Securities and Markets Authority (ESMA), and more use of qualified majority voting with no country having a veto. This was underlined later in the week when the EU’s “Big 6” struck a deal on financial market regulation.

In short, these are more reminders that the EU that some want the UK to rejoin would be very different (bigger and less democratic) from the one we left, and we would have to rejoin on different (even worse) terms.

Thursday 28 May

“NEETs” day. The latest ONS data showed that more than one million 16-24 year-olds are not in education, employment or training, as a report by Alan Milburn warned of a “lost generation”.

This is a huge topic and deserves far more thought. But for what it is worth, the biggest single problem may just be the overall weakness of the economy and especially the high level of uncertainty. This has put a freeze on recruitment and happens to be hitting entry-level jobs particularly hard. The growing use of AI may also be a factor for some jobs.

This has inevitably led to demand for even more state intervention. But Ministers should remember the principle of “first do no harm”. One of the best things that the government can do now would be to reverse some of the policies which have made the underlying problems worse.

In particular, the additional costs faced by businesses are actively discouraging them from employing young people. It is surely no coincidence that some of the biggest job losses have been in sectors, notably hospitality and retail, where labour costs have risen the most.

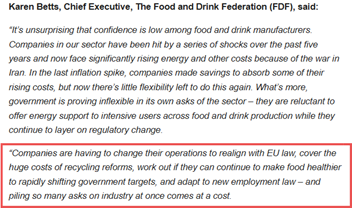

This is part of a wider problem. Thursday also saw the publication of a pretty damning report from the Food and Drink Federation. The comments below make the points well. (Note that the additional costs include the impact of the proposed new SPS agreement as part of the UK-EU “reset”, which will require UK firms to realign with EU laws.)

Friday 29 March

By the end of the week, Keir Starmer, Andy Burnham and Wes Streeting had all responded to Tony Blair’s essay. There was a handy summary here from Julia Willemyns, which saved me from writing one.

One thing that stuck me was the emphasis on rising inequality, which you might expect from Labour politician but is poorly grounded in reality. The data actually shows that most measures of inequality have been flat for two decades – or have fallen.

Here, for example, is a chart of the UK’s Palma ratio. You can find others in this summary from the ONS, or in the international comparisons provided by Our World in Data.

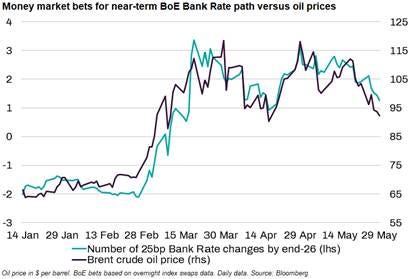

Finally, it was at least a better week for the bond markets. The yield on 10-year gilts is now back at around 4.8%, having touched 5.2% earlier in the month. The key driver is fading fears of inflation as the oil price has dropped on hopes of a resolution to the crisis in Middle East. As this chart from Kallum Pickering shows, this has also been the key driver of market expectations for official interest rates.

For now, hopes of a US-Iran deal are trumping any worries about UK political risk. Or put another way, the bond markets are “in hock” (©️ Andy Burnham) to oil prices…

Have a great weekend, and COYG!

You can follow me on X (formerly Twitter) @julianhjessop and on Bluesky.

I also post regularly on Substack