Although not as bad as the dark days of the 1970s, the UK economy is heading for a period of falling activity, rising inflation, and higher unemployment. Government tinkering with prices won’t help.

By overwhelming popular demand (Sid and Doris Bonkers), I’m launching a weekly wrap of the key points made in my social media posts on the UK economy. This includes a selection of my favourite charts. Future editions will add more on the markets and occasionally on the politics too.

IMF forecast revision (Monday 18 May)

The week started on a brighter note with the release of the IMF’s latest Article IV Consultation with the UK. The headlines focused on the upward revision to the 2026 GDP growth forecast, from 0.8% (in the April World Economic Outlook) to 1.0%. But this update simply reflected the better data for the first quarter (“old news”), rather than any improvement in the outlook for the rest of 2026. The bigger picture is that growth is still expected to slow, from 1.4% last year, and the near-term risks are clearly on the downside.

The IMF did have some kind words for the government’s economic and fiscal policies – a reminder of why investors would prefer the status quo rather than a change in the occupant of either Number 10 or Number 11. Rachel Reeves is at least the “devil that the markets know”. Andy Burnham’s apparent recommitment to her fiscal rules has therefore gone down well.

But the IMF’s comments below on the longer-term fiscal risks was more interesting. Will any political party be brave enough to start a public debate on the triple lock, or more charging in the NHS? I fear they will not…

Labour market data (Tuesday 19 May)

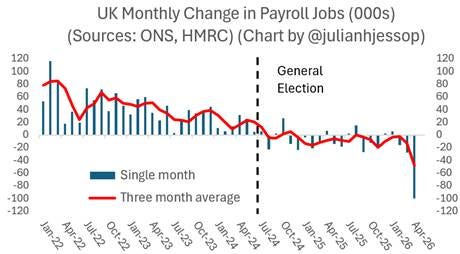

This is when the week started to take a turn for the worse. In particular, payrolled employment slumped by another 100,000 in April, after a downwardly revised fall of 28,000 in March.

The ONS noted that the April data are particularly prone to revision (but this could be up or down), while others have emphasised the impact of Middle East uncertainty (surveys do suggest that recruitment is being put on hold). However, payrolled employment has been persistently weak since 2024, and government policies which have pushed up labour and other business costs are a huge drag.

Elsewhere in the report, the headline unemployment rate, which was the average in the three months to March, ticked up from 4.9% to 5.0%. However, the single month figure for March alone was 5.5%. These single month figures are relatively volatile, but there’s more bad news to come.

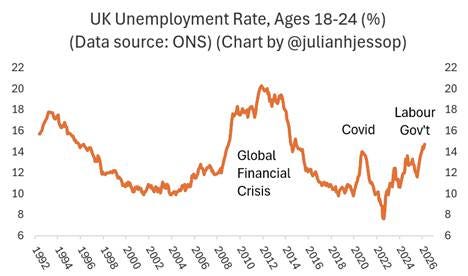

The youth unemployment numbers are already dire.

It was well-nigh impossible to find any silver linings in the report, but here are two. First, the weakness in the jobs market and the further slowdown in wage growth should at least kill off any chance of a rate hike from the Bank of England (private sector earnings growth excluding bonuses eased from 3.2% to just 3.0%).

Second, unless output collapses too, the payroll-based measures of labour productivity will look a little better. But this will be of no comfort to those losing their jobs.

Inflation (Wednesday 20 May)

The news on inflation was a little better than expected, as the CPI measure fell back to 2.8% in April, from 3.3%. This was due to the reduction in the Ofgem cap on domestic energy bills (thanks in part to the government’s decision to transfer some costs to general taxation), helped also by an unexpected fall in food price inflation. The core measure was down too, perhaps flattered by the timing of Easter.

Unfortunately, this may now be as good as it gets for the rest of the year. The CPI measure is still likely to rise towards 4% in the coming months as more of the cost increases caused by the Middle East crisis feed through the pipeline.

However, two factors should cap the upside. One is that demand is weakening and the labour market is continuing to deteriorate. This means that corporate pricing power is limited and the risks of second round effects, including a wage-price spiral, are minimal.

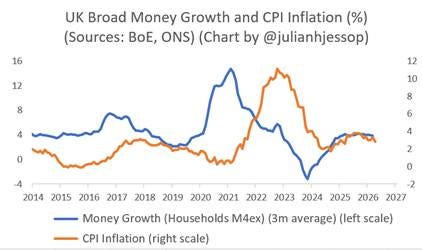

The second factor – just as important but too rarely discussed – is that the growth in broad money has been subdued. This is in sharp contrast to the rapid acceleration in money growth in 2021 which helped to fuel the surge in inflation in 2022.

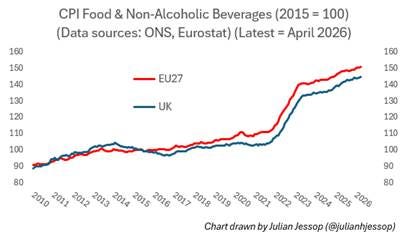

In the meantime, many commentators continue to blame the surge in food prices on Brexit. This next chart shows what has actually happened to food prices in the UK and in the EU, each indexed to their respective levels in 2015. The big picture is that food prices have surged across Europe, but by a little less in the UK than in the EU.

Flash PMI survey (Thursday 21 May)

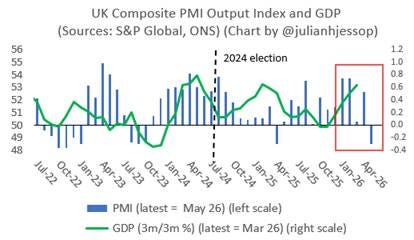

This survey sent the clearest signal yet that the UK economy is heading for a period of stagflation, or at least “stagflation-lite”.

The slump in the Composite Output Index to 48.5 in May confirmed that the burst of growth in Q1 has already evaporated. GDP is likely to contract in Q2, reflecting both the global fallout from the Iran war and mounting political uncertainty at home.

The inflation numbers were alarming too. Here is a good chart from the PMI report (though I think it would be even better if the scales were swapped so that CPI inflation is on the right…). At face value the PMI is consistent with inflation topping 6%. I don’t think it will get quite that far, but the upside risks are obvious.

Consumer and retail data (Friday 22 May)

The GfK measure of UK consumer confidence rose two points in May, but the devil is in the detail. Lower and middle income households reported steep falls, presumably because they are more likely to lose their jobs and less likely to have savings to tide them over.

“For those earning £14,500 to £24,999, for example, the May score is -33, a 19-point fall below the -14 seen in April. Similarly, there is also a steep fall within the average household income group (£35,000 to £49,999), with a 10-point drop from -17 to -27.” (Source: GfK Consumer Confidence Barometer powered by NIM)

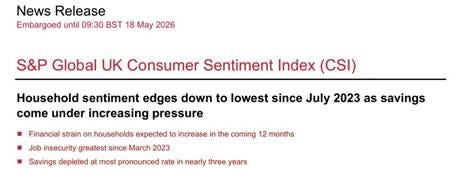

The headlines from the alternative S&P Global UK Consumer Sentiment Index (released on Monday) told the story a little better.

The fragility of consumer confidence is is already beginning to show through in the official data on retail sales. Volumes fell by 1.3% in April, mainly due to a slump in sales of motor fuel (unwinding the jump in March). But sales excluding fuel also fell, by 0.4%. The bigger picture here is that retail is starting to roll over as the boost from real income growth fades and confidence falters again.

The public finances (Friday 22 May)

It is very early days, but the public finances also made a bad start to the new financial year. The UK government borrowed £4.9 billion (or 25%) more in April than in the same month a year ago. Spending was up £7.6 billion, while revenues rose by just £2.7 billion.

Remember too that the budget deficit only fell last year because of a large increase in the tax burden. As the IMF noted at the start of the week, the scope for any further tax increases is severely limited.

Cost of living measures (all week)

Over the course of the week the government announced a number of increasingly desperate measures to tackle the cost of living crisis, including an extension of the 5p cut in fuel duty, more cuts in the UK’s tariffs on imported food and other items, “free” summer bus travel for kids, discounted attractions and a temporary VAT cut on children’s meals out.

Again, there is a Brexit angle here. It would not be possible to cut tariffs unilaterally if the UK were still part of a customs union with the EU. Members of the EU also have much less freedom to cut VAT.

Overall, though, these measures will not amount to much. “Bread and circuses” was one dismissive response. The liberal use of “free” is also misleading, because the taxpayer will be picking up the bill.

On a lighter note, the difficulty of policing the definition of a “children’s meal” has at least raised a few smiles (hat tip to Robert Colvile for “Try Uncle Kranky’s Krazy Kaviar”). Indeed, these wheezes are reminiscent of previous gimmicks, such as Rishi Sunak’s “Eat Out To Help Out” scheme.

There were reports too that the government was revisiting the idea of “voluntary” caps on the prices of essential foods. Rishi Sunak also floated something similar when he was Prime Minister in 2023, before backing down.

One difference this time is that a cap might have been linked to regulatory concessions, such as relaxing or delaying new packaging rules and levies. But those measures are only a small part of the extra costs that government has imposed on businesses, on top of the fallout from the Iran war.

And just to make it worse, it looks like the government is about to add to these costs (“Food prices to rise as £2bn packaging tax goes ahead”). Cue Robert again…

Crucially, the supermarket sector is already highly competitive, and retailers work on tiny margins. Price caps are only likely to reduce both the supply and quality of the items that are capped, while raising the prices of others.

The government now seems to have seen sense and backed down again. But for a complete demolition of supermarket price controls, try this piece by Ryan Bourne.

The reality is that clumsy government interventions have already done more harm than good. The direction of travel under Labour is towards even more intervention in wage and price setting. This is already costing jobs, reducing the supply of rented housing, and distorting the market for energy.

In my view. the government should focus on freeing up the supply side of the economy and easing the constraints that are contributing to higher prices, rather than tinkering any further!

You can follow me on X (formerly Twitter) @julianhjessop and on Bluesky.

I also post regularly on Substack