Keir Starmer’s government is wasting its remaining time and your money playing at being a tech investor, while failing on everything from job security to national security.

Welcome to the latest weekly wrap of the key points from my social media posts, with comments on the UK and global economies, the markets, and occasionally on politics too.

Sunday 7 June

The week began early as a guest on Matthew Wright’s morning show on LBC to discuss Peter Kyle’s plan to take bigger stakes in Britain’s next tech giants. I ended up writing a blog “Politicians should not play at being ‘tech bros’ with taxpayers’ money”, whose title pretty much speaks for itself.

In particular, the British Business Bank’s much-hyped £25 million (yes, “million”) investment in the Octopus spin-off Kraken is a perfect example of spin over substance. The plan is supported to be about “betting big” and “picking winners”. But the UK government’s stake was only a tiny part of a $1 billion fundraising round and Kraken was already a success.

More importantly, the whole approach is fundamentally flawed. The government should focus on creating the conditions in which businesses can thrive and private investors want to invest, without taxpayer support.

Monday 8 June

The KPMG and REC UK Report on Jobs for May provided another example of the benefits of a more flexible labour market. The survey showed that increased economic and political uncertainty means firms are reluctant to make permanent hires, but they are at least employing more people on temporary contracts.

Unfortunately, this flexibility is being undermined by the government’s increasingly clumsy interventions, notably the jobs-destroying “Employment Rights Act”. REC’s Neil flagged up the new rules on zero-hours contracts as one concern, but there are many others.

Meanwhile, the BBC aired a debate between the Sunday Times’ David Smith and myself on the economic impact of Brexit ten years on, which you can listen to here. My more positive points didn’t make the cut, but at least I was able to have another go at the claims of a 4-8% hit to GDP. (For more, see my “Explainer – debunking the dodgy stats used by Project Rejoin”.)

Tuesday 9 June

Bloomberg Economics also published some new analysis of the impact of Brexit, which had something for everyone. My own take was that the report was still too negative, but the analysis was helpful in countering the more extreme claims about both the costs of leaving the EU and the benefits of rejoining.

In particular, the Bloomberg economists’ central estimate was that the long-term hit will be 2.5% of GDP, still a significant amount but much lower than other estimates. What’s more, there would be little to gain from closer realignment.

For example, rejoining the Customs Union would add just 0.4% to GDP, while severely limiting the UK’s ability to run its own trade policy. A Swiss-style arrangement might add 0.8%.

Bloomberg economists also demolished the NBER claim that UK GDP was already 8% smaller than it would otherwise have been, which they rightly described as “misleading”.

They came up with a lower estimate of 3.4% for the impact to date by stripping out Ireland and “adjusting the US growth trajectory to reflect pre-2016 levels of outperformance”.

In my view, though, these “top down” estimates are all flawed, because they simply cannot strip out the impact of Brexit form everything else that might have affected the relative performance of different economies before and after 2016.

Bloomberg’s 3.4% is too high, partly because it still includes data from countries like Italy and Spain whose post-2016 growth has also been flattered by local factors (notably the rebound from the euro debt crisis of the early 2010s and exceptional fiscal stimulus).

There is also no discussion of the Brexit benefits – including smarter regulation and savings on contributions to the EU budget – which should build over time.

Finally, it is worth noting that even Bloomberg economists are now revising down their previous estimates. Back in 2023 they claimed that Brexit was costing the UK 4% in lost output every year, which was around £100 billion at the time. Hopefully the usual suspects will not stop citing those outdated figures, but I bet they won’t…

Wednesday 10 June

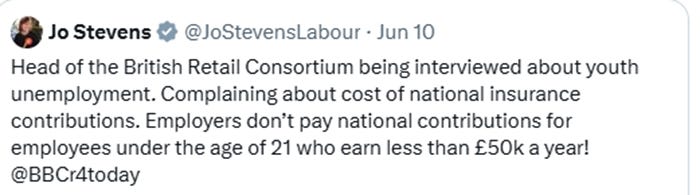

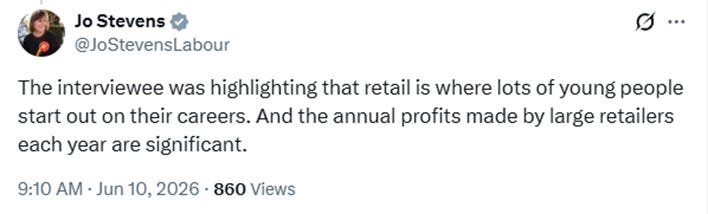

I found myself siding with the British Retail Consortium (BRC) against this point made by Labour’s Secretary of State for Wales, Jo Stevens.

This is misleading, because the usual definition of “youth unemployment” and “young people not in education, employment or training (NEET)” covers people from the ages of 16 to 24, rather than stopping at 21. The BRC’s concerns about the impact of the increases in employers NI are therefore still valid.

The Welsh Secretary also posted…

The suggestions that supermarkets are highly profitable is, of course, well wide of the mark. The large chains may make what appear to be large profits in cash terms, but these are small compared to the size of the business (e.g. relative to turnover, capital employed, or employee numbers). In other words, they run on very tight margins.

Nothing personal against the Minister here, but the level of economic and business knowledge of MPs continues to disappoint.

Thursday 11 June

The European Central Bank hiked the euro area’s key interest rate by ¼% to 2¼%, as expected, with more tightening on the cards in the coming months. This fuelled some speculation that the Bank of England might soon follow suit (the announcement is on Thursday 18). This still seems unlikely, given the higher starting point (3¾%) and the more limited risks of “second round” effects in the UK, but I will return to this early next week.

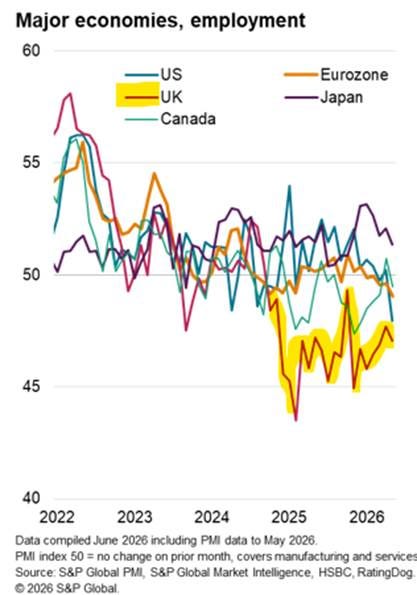

In the meantime, the latest PMI surveys illustrate the relative weakness of the UK labour market. Some are trying to blame rising unemployment on global shocks. But the PMIs show that the UK is suffering “an especially steep pace of job cuts”, which began around the time of Rachel Reeves’ first Budget in the Autumn of 2024.

But the big news of the day (and the week) was John Healey’s resignation as Defence Secretary. This may well be the fatal blow to Keir Starmer’s premiership, leaving Andy Burnham to deliver the last rites. Indeed, the whole episode has symbolised the chaos at the heart of this government, including the inability to deliver a credible plan and the lack of leadership from No.10.

But my turf is supposed to be economics, so I wrote a piece with three quick points on the economics of defence spending. Here is just a brief summary.

First, defence is a textbook example of a ‘public good’ which cannot be left solely to private markets. But this also requires a lot more political will, which is currently lacking.

Second, more defence spending is not necessarily good for growth. The overall impact will depend on many factors, including how the additional spending is financed, and whether there is enough spare capacity to meet the additional demand.

Nonetheless, there may be a helpful regional dimension here. An increase in defence spending will probably favour regions outside London and the Southeast, supporting areas with more military bases and which are more dependent on manufacturing than services.

Third, the money will have to come from somewhere. The best solution, of course, would be to fund increased defence spending from savings elsewhere in the government’s budget, focusing on welfare spending and rowing back from areas like “net zero” and “industrial strategy” which should be left to the markets.

As a stop gap, another option would be the issuance of “defence bonds”. These could be similar to the existing “green gilts”, or the saving schemes that were run during the two World Wars. But a more imaginative proposal is to issue special zero-coupon bonds where any capital gains would be exempt from inheritance tax.

These bonds would not pay regular interest – an upfront saving for the government. Instead, the bonds would be sold for less than their face value, so investors would be compensated by the uplift when the bonds mature.

Admittedly, more borrowing to pay for defence would still be more borrowing, and these bonds could just defer the costs. But demand for new savings products that are both “patriotic” and free from inheritance tax is likely to be high, which should reduce the average cost of borrowing.

I can’t yet say I’m sold on this idea, but it is at least worth considering.

Friday 12 June

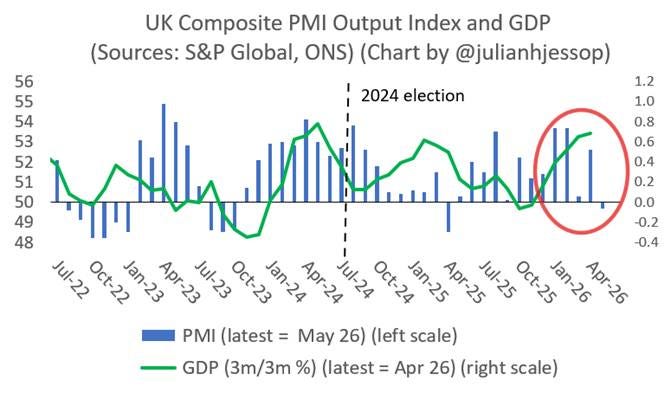

The UK GDP figures for April are too soon for any big hits from the Iran war or the political turmoil at home. For the record, the economy contracted by 0.1% m/m, but the strength of February and March still saw the 3m/3m rate tick up to 0.7%.

Unfortunately, we already know this upswing is not going to last. Almost every business and consumer survey is signalling a sharp slowdown in the second quarter, with the economy likely to stagnate at best. The composite PMI (covering services and manufacturing) is just one example.

The PMI for the construction sector has been even weaker. This may seem hard to square with the apparent strength in the GDP data, where construction output jumped by 1.6% 3m/3m. But this was flattered by repair and maintenance, with new work still in a prolonged slump. The latest RICS survey also shows that sales activity in the housing market remains in the doldrums.

And finally…

Good news for those uncertain whether to blame the defence spending fiasco on the Prime Minister or the head of the Treasury… you can do both!