The strong growth in UK GDP reported in the first quarter will not be sustained. At best the economy is set to stagnate again in the second quarter, and possibly in the third too.

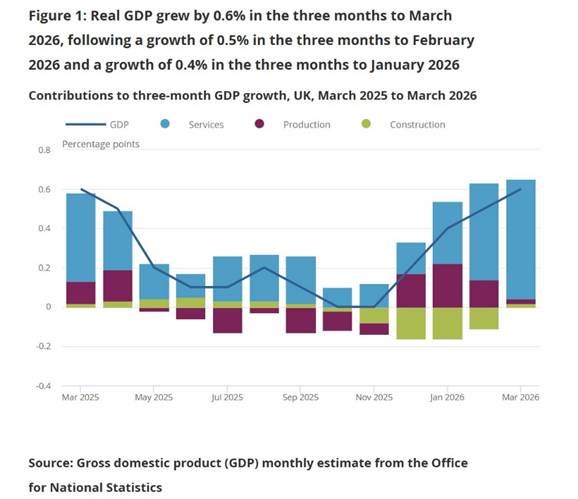

Some good news for a change. The first official estimate for the first quarter confirmed that the UK economy made a flying start to 2026, with growth of 0.6% q/q (in both headline and per capita terms). This was partly a rebound from the weakness in the run up to last November’s Budget, when damaging speculation had held back activity. But at least the Budget itself was not quite as bad as feared.

Unfortunately, we have been here before: the first quarter has seen the strongest growth in each of the last four years, followed by a marked slowdown.

and created by Julian Hess.

AI-generated content may be incorrect.")

This may partly reflect some problems with the number themselves. The statisticians at the ONS (to their credit) have acknowledged concerns over the reliability of the seasonal adjustments, and they are working to improve them.

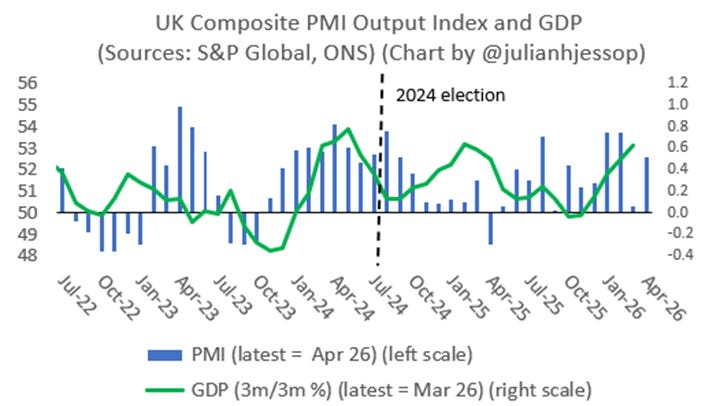

Nonetheless, the earlier improvements in many business and consumer surveys suggest that most of the 0.6% increase in GDP was genuine.

But looking forward, many of the same indicators are already pointing to a much weaker second quarter as the fallout from the crisis in the Middle East starts to hit.

For now, manufacturing and most services appear to be holding up well, perhaps benefitting from demand brought forward to beat the expected supply shortages and price rises.

However, activity in other sectors is starting to weaken sharply. Examples from the early April data include:

- The BRC reported a big year-on-year fall in retail sales – mainly due to the variable timing of Easter, but rising uncertainty and falling confidence are weighing too.

- The latest BDO tracker of High Street sales was also poor (“High street suffers worst April sales performance in a decade”).

- The RICS survey shows activity in the residential housing market was already taking a hit in April from higher mortgage rates.

- The S&P Global UK Construction PMI suggests activity tanked again “Steepest decline in construction output since November 2025”).

- The KPMG and REC Report on Jobs still suggested that the slump in the labour market is easing, but recruiters also report that the preference for temporary rather than permanent hires has been strengthened by the additional uncertainty from the Middle East.

The mounting political uncertainty at home will not help either. Nervousness in the financial markets over the fate of the Prime Minister is adding to the upward pressure on borrowing costs – and for good reason (as I argued here).

The lack of any meaningful measures to boost growth in the King’s Speech is a worry too. Instead, the government chose to double down on clumsy state interventions which are holding the economy back.

In short, the strong growth in UK GDP reported in the first quarter will not be sustained. At best the economy is set to stagnate again in the second quarter, and possibly in the third too. But at least there was some positive momentum before the Iran war, so it’s not all bad news.

You can follow me on X (formerly Twitter) @julianhjessop and on Bluesky.

I also post regularly on Substack.