In a recent interview with the Financial Times, former Bank of England Governor Mark Carney made the striking claim that ‘in 2016 the British economy was 90% the size of Germany’s. Now it is less than 70%’. This claim is garbage, for two reasons. Unfortunately, it is just one of a tsunami of fake statistics which is helping to turn public opinion against Brexit.

Indeed, Mr Carney went even further on the Radio 4 Today programme last Friday, when he appeared to blame the current surge in UK inflation and the latest increase in interest rates on the decision to leave the EU.

Let’s start with the Germany comparison. Mr Carney has attempted to contrast the sizes of the two economies over time using the prevailing market exchange rates. This in itself is dodgy. But even his own numbers are wrong, because he has mistakenly compared real (inflation-adjusted) GDP in the UK with nominal GDP in Germany.

This howler is revealed by the figures in a follow-up tweet in which Mr Carney showed his working. He stated that UK GDP was £2.1 trillion at the start of 2016, or 94% of Germany’s sterling-equivalent of £2.2 trillion, and that it is now £2.17 trillion, or 70% of Germany’s £3.10 trillion.

Eagle-eyed readers may have spotted that the percentages here (‘94%’ and ‘70%’) are different from those in the FT interview (‘90%’ and ‘less than 70%’). But there is a more serious mistake. According to Mr Carney’s numbers, the German economy has grown by more than 40% in sterling terms since 2016, whereas the UK economy has grown by less than 4% (you do the maths!). This obviously cannot be right, even allowing for swings in the value of the pound.

Digging further, it looks like Mr Carney has used annual data for 2015 and 2021. The German numbers are pretty close to the national data on nominal GDP, and appear to be correctly translated into sterling. However, his UK numbers match the official ONS data on real GDP. In other words, he is comparing ‘apples’ and ‘pears’, and this biases the comparison in favour of Germany.

It is worth noting too that we now have UK and German data for the first half of 2022. On this basis, and using the right ONS data on nominal GDP, I estimate that the UK economy has ‘shrunk’ from about 87% the size of Germany’s before the EU referendum to about 76% now. Alternatively, if you keep it simple and just look at the World Bank database, UK GDP in current dollar terms fell from 88% of Germany’s in 2015 to 76% in 2021. Either way, the fall is only half as large as Mr Carney claimed.

Of course, these figures still suggest that the UK economy has substantially underperformed Germany’s since 2016. But that would still be the wrong conclusion.

Recall that Mr Carney attempted to compare economies using market exchange rates. At best, this approach is misleading. Other economists have been less charitable. Jonathan Portes has called Mr Carney’s claim ‘nonsense’, while Ashoka Mody has dismissed it as ‘complete bulls***’.

There are three main problems here. First, market exchange rates can be volatile. As Jonathan Portes has put it, ‘the pound has risen by almost 10% against the dollar since the Truss nadir. Has the UK economy really grown by almost 10% relative to the US in a few weeks?’.

Second, the relative importance of exchange rate movements depends on the degree of openness of a economy to international trade. In other words, a 10% rise or fall in the value of the local currency will have a bigger impact on an economy – and real incomes – where imports and exports account for a larger share of GDP.

For these reasons, economists generally prefer to use Purchasing Power Parity (PPP) exchange rates, which allow for a like-for-like comparison of living standards in different economies.

Third, context matters. Sterling did fall sharply in 2016, but it has since been relatively stable (at least against the euro). The decline, which began well before the referendum, also did little more than reverse the rise between 2013 and 2015. (The chart below shows the Bank of England’s trade-weighted index against a basket of currencies, set at January 2005 = 100.)

It is probably right to attribute some of the fall, especially in mid-2016, to the shock referendum result. But the pound may well have weakened anyway, even if the precise timing and extent might have been different. Many commentators – including the IMF – were already raising concerns in 2015 that sterling was looking heavily overvalued, based partly on an unsustainably large current account deficit.

This is not to say that swings in market exchange rates can be ignored. The fall in the pound in 2016 did contribute to a (small) rise in UK inflation in the following year, by making imports more expensive. Nonetheless, comparing GDP using market exchange rates is still the wrong way to show this.

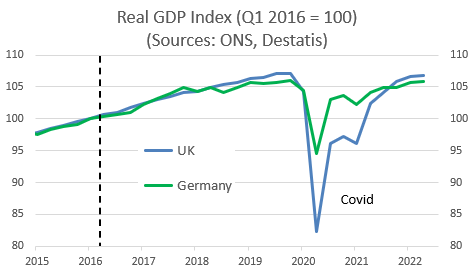

Instead, you should just use the national data on real GDP, which will pick up any impact on inflation, as well as changes via other channels such as trade and investment. Despite the adverse effects of Brexit – and there have clearly been some – the UK economy has grown by about the same amount in real terms as Germany’s since 2016 (albeit with a bigger hit from Covid).

Does any of this matter? Regrettably, it does. The original sin may have been Mark Carney’s, but his dodgy claim in the FT interview was like catnip to Remainers and gleefully retweeted by all the usual suspects. More worryingly, it was taken as gospel by high-profile commentators, such as Edward Luce, Jonty Bloom, and Clare Foges.

Mr Carney’s interview with the Today programme was just as weak. The reality is that UK inflation is similar to the average in the euro area, and that UK official interest rates of 3% are roughly where they usually are – somewhere between the euro area (currently 2%) and the US (4%). If the fallout from Brexit is playing any part here, it is only a small one.

In short, sloppy analysis must not be allowed to feed the false narrative that Brexit has been an economic disaster. It is particularly disappointing when ‘public servants’ are at it too.

Julian

Very interesting. Let me digest and revert. Meantime, I see both sides of the basic PPP vs current rates disagreement Carney/Portes. Could it be that we are mixing two concepts here … Carney more of a ‘standard of living’ point of view? PG

LikeLike

Thanks. PPP and market exchange rates are indeed two different concepts, but if you are concerned about standard of living or real incomes you should surely use the former (this is what the ‘purchasing power’ in PPP is about).

LikeLike

Interesting analysis.

LikeLike