Investors are mainly being spooked by global inflation fears, not UK politics. But the additional uncertainty created by the crisis in the Labour government is definitely not helping!

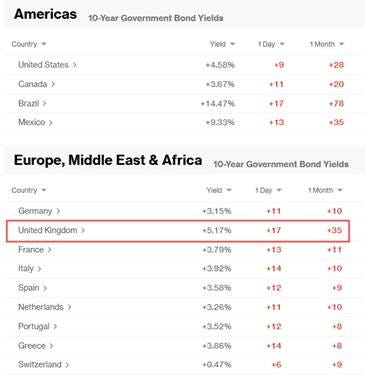

Once again, UK government bonds (aka gilts) are making the news again, and not in a good way. The yields on these bonds can be read as the interest rates that the government has to pay on new long-term borrowing. Since late February, the yield on the 10-year gilt has jumped from around 4.4% to nearly 5.2%.

So, what’s going on? The first point to stress is that this is part of a global move, triggered by the Iran war and the resulting surge in the cost of crude oil and other commodities.

The moves today (Friday 15 May) illustrate the importance of putting what is happening in the gilt market in the wider context. As the Bloomberg summary below shows, bond yields have jumped everywhere, which reflects the global inflation fears. Indeed, other countries are seeing some worrying headlines too, notably in the US where the 30-year Treasury yield has topped 5% for the first time since 2007.

Nonetheless, it is also notable that the cost of UK government borrowing is rising more than most – and from a much higher starting point.

There is still a myriad of UK-specific factors at play here. The second point to stress is that the higher cost of UK government borrowing relative to other countries is only partly due to the emerging crisis within Labour.

Instead, this is mainly about the UK’s relatively high inflation and official interest rates, which were already set to be higher for longer than in other countries. There are also some more technical factors, notably the UK’s larger stock of inflation index-linked debt and the active sales of bonds by the Bank of England under the policy known as “Quantitative Tightening”.

However, the additional political uncertainty is a significant factor too. This is not because financial markets are seeking to “constrain democratic choice” or exercise “political power” in the UK, as some on the far Left have suggested. That claim is even more nonsensical if you look at what is also happening in the rest of Europe, or the US.

In reality, it is perfectly normal for investors in any market to require a higher return when lending is perceived to be riskier, for whatever reason. This is just basic economics and has nothing to do with politics, or ideology.

In this case, investors are understandably worried that new leadership in the UK, or simply a lame duck in Number 10, will mean more spending, more borrowing, more inflation, and more taxes, as well as other policy interventions that encourage more capital flight. This makes holding UK assets riskier, and hence investors demand a bigger premium for the additional risk.

Put another way, lenders prefer to know who they are lending to, and what the money will be used for. If you don’t like that, don’t try to borrow so much from them!

Worse still, any crisis of confidence is unlikely to be contained to the bond market. Sterling will surely suffer further too, and mortgage costs will jump if official interest rates are expected to be higher for even longer.

It is frankly anybody’s guess what happens next within Labour. Even some of the key participants seem to have no idea.

For what it is worth, I suspect a smooth Burnham coronation may now be the best (or least bad) scenario for the markets. However, he would still have to do a lot more to reassure investors, especially on fiscal policy. The worst case is that he loses the Makerfield byelection (mostly likely to Reform) and the Labour civil war escalates even further.

The next (slightly more reassuring) point is that the surge in gilt yields only affects the cost of new borrowing, so there would only be a large hit to the public finances if it is sustained. But a longer period of higher short rates (the official interest rate set by the Bank of England) would have a more immediate impact, including on the wider economy.

Moreover, in contrast to what the media often says, it is the expectation for short rates, not gilt yields, that determine the cost of fixed-rate mortgages. (To be precise, 2-year and 5-year mortgage rates are priced off 2-year and 5-year swap rates, not gilt yields, even though all may sometimes move together.)

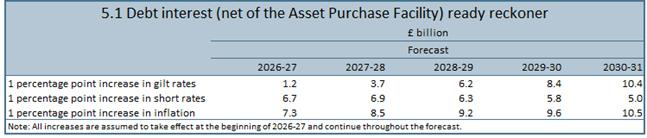

Finally, the OBR’s debt interest ready reckoner gives a sense of the numbers involved.

There is a lot to unpack here, but in brief…

i. The annual cost of higher gilt yields will rise over time as more new borrowing is financed at the higher rates. In year one a 1%-point (100bp) increase in gilt yields would cost just over £1bn, rising to more than £10bn in year five.

ii. The impact of an increase in short rates comes through more quickly (the Bank financed its purchases of gilts under “Quantitative Easing” by creating deposits on which it pays interest at the Bank rate). A 1%-point increase in short rates would cost nearly £7bn in year one, but then fall (mainly because the Bank is running down its holdings of bonds via “Quantitative Tightening”, though this process also creates capital losses not included here).

iii. An increase in inflation also has a direct impact on debt interest payable, because of the UK’s relatively large stock of inflation index-linked debt. This effect is large and builds over time (though most of the money here is not actually paid out until the bonds mature, which could be many years in the future). A 1%-point increase in inflation would cost more than £7bn in additional debt interest in year one (though higher inflation would actually help the public finances in other ways, again not included here).

iv. Altogether, a sustained 1%-point (100bp) increase in gilt yields, short rates and inflation could add around £15bn to the annual debt interest bill in year one, rising to around £26bn in year five.

The upshot is that a combination of higher debt servicing costs and weaker economic growth could easily wipe out the government’s fiscal headroom, requiring further painful choices in the next Budget.

This leads to a worrying conclusion. A key reason for the weakness in the UK economy in the second half of last year was the damaging speculation in the run up to the November Budget. This year we have both the fallout out from the Iran war and the new uncertainty created by more Labour chaos.

The jump in gilt yields may not be an immediate threat to financial stability. But it does reflect deeper underlying economic and fiscal problems that cannot be solved by even more borrowing, whatever some on the Left may wish.

You can follow me on X (formerly Twitter) @julianhjessop and on Bluesky.