Ever since the 2016 referendum, Brexit pessimists have been highlighting the damage that they think has already been done to UK GDP by the vote to leave. This narrative is looking increasingly tired. Indeed, last year the UK economy actually grew faster than its peers in the rest of the EU. Now that Brexit is finally happening, this outperformance should continue.

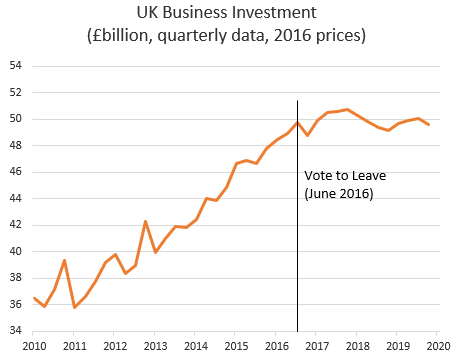

To be fair, the needlessly prolonged Brexit uncertainty has been a drag on growth. The initial fall in the pound raised the cost of imports, while business investment has stagnated (as the chart below shows). But the overall impact has been (much) smaller than some commentators would have us believe.

In particular, there have been many attempts to quantify the impact of Brexit by comparing the UK’s growth to that in the rest of the G7, or other countries whose performance has been similar to ours in the past. These studies have typically concluded that the level of UK GDP is now around 3 per cent lower than it would otherwise have been, or a shortfall of around £60 billion a year.

But these studies are also riddled with problems. Their biggest weakness is the assumption that any difference in the relative performance of the UK since 2016 is due to Brexit. In reality, there were plenty of good reasons why the UK would have slipped down the growth league tables anyway, regardless of the referendum result.

After all, the UK had been one of the two fastest growing economies in the G7 in every year from 2013 to 2016. That was unsustainable, with the euro-zone in particular overdue a period of catch up. What’s more, any international comparison is dominated by what has happened in the US, where the economy has benefited from a substantial fiscal boost.

The upshot is that estimates of a GDP loss of 3 per cent are surely exaggerated. My own view is that a more credible figure would be no higher than 2 per cent, and probably less, considering the continued strength of the labour market. Contrast that with the Treasury’s warnings that the level of GDP could be as much as 6 per cent lower by now, and that unemployment would soar…

Whatever the precise number, though, the more important point is whether this hit is permanent and a sign of worse to come. It may be too soon to see the full impact of Brexit until we have actually left, but this also applies to potential benefits as well as costs.

Indeed, the initial damage already appears to be reversing. Sterling has risen by about 6 per cent on a trade-weighted basis since Boris Johnson became Prime Minister. Obviously, there is still a long way to go to reverse all the fall after the 2016 referendum. However, that may not be such a bad thing, given the advantages of a more competitive currency.

Business investment is also set to rebound, starting this year. Brexit pessimists will argue that spending has been held back by the reality of the damage that they believe leaving the EU will do, not just uncertainty about the process. They will also emphasise that the UK is still in a transition period where not much has actually changed, and that the hard work in negotiating a new relationship with the EU is only just beginning.

Nonetheless, there is now less uncertainty about Brexit than there was before the election. We know for sure that the UK is leaving the EU and there is much greater clarity about the timing of the next stages. Those companies most directly affected by Brexit will continue to focus on the details that are crucial to them. But Brexit will no longer dominate the national news as it has for the last three years, depressing business and consumer confidence and diverting the government from tackling other issues – from infrastructure spending to social care – that probably matter more to most people.

It is also wrong to focus solely on the negotiations that still have to be completed with the EU. Businesses are already learning more about the likely shape of other post-Brexit arrangements, including new policies on migration and on tariffs with the rest of the world. There is now strong momentum behind a US-UK trade deal too.

Even if Brexit does has some negative effects for some companies in the long run, these companies will at least soon know more about what they will be dealing with in terms of new trade barriers or limits on movement of workers, and hence how to respond.

For now, this more optimistic view may appear be largely speculative. But there is plenty to support it, both in the surveys and the official data. There is little evidence of any long-term damage to the attractiveness of the UK as a destination for foreign investment. Indeed, some companies are relocating activities here to avoid any potential barriers to doing business in the UK itself. The short-term business surveys are also already reporting a jump in confidence, including investment intentions.

Admittedly, this is at least as much a ‘Boris bounce’, reflecting relief at the election result, but most surveys also show a reduction in worries about Brexit as well. In any event the two are not entirely separate: one important way in which Brexit uncertainty has held back the economy is that it has distracted policymakers from domestic problems.

What’s more, the renewed outperformance has already begun to show through in the hard numbers. The headlines have focused on the weakness of the UK economy at the end of last year, when GDP was flat in the fourth quarter. But it was also flat in Germany, and fell outright in France, Italy and Japan. Taking 2019 as a whole, the UK grew faster than all four of these countries, and was vying with Canada for second place again in the G7, behind the US.

In short, Brexit uncertainty is not going to disappear overnight. Nonetheless, almost all the available evidence supports the view that the economy is now heading in the right direction again, with a rebound in investment setting up another year of outperformance in 2020.

This piece was first published by Global Vision