(This piece was written on 27th November. Since then the new survey evidence has suggested that the hit to GDP from the November lockdown was smaller than expected, which is obviously consistent with the relatively upbeat message here.)

For what it’s worth, I’ve been comparing my UK economic forecasts with those of the OBR. There is a much more positive story than the Chancellor told in Wednesday’s Spending Review 2020. Let’s start with the near-term outlook…

The OBR assumes that the economic impact of the second lockdown will be ‘three-fifths’ that seen during the first, when GDP fell by 25% in March and April. This means that the second lockdown would take the level of GDP back to 15% below its pre-Covid peak.

Given that monthly GDP was 8.2% lower in September than February, and assuming little change in October, this is consistent with a fall of around 7% m/m in November, which is what’s in the OBR’s ‘central forecast’. This seems about right to me, based on early survey evidence such as the flash PMIs.

But thereafter, the OBR’s ‘upside scenario’ (summarised below) is closest to my view.

The economic costs of being in either Tier 1 and 2 are small. Your social and family life may be constrained, but most economic activity can continued as normal.

The main difference in Tier 3 is the additional hit to the hospitality sector, but this is only a small part of the overall economy: ‘accommodation and food services’, which includes pubs and restaurants, is about 3% of GDP.

Hospitality is relatively labour-intensive, but the blow here should be cushioned by the #furlough scheme. The latest ONS Business Impact of Coronavirus Survey suggests that the number of people on furlough has already jumped from about 2½ million to 4 million.

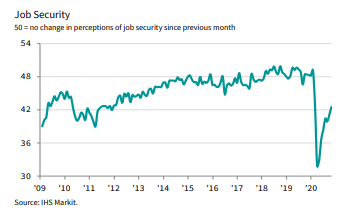

Despite this, or perhaps helped by the extension of the furlough scheme, household perceptions of job security actually recovered further in November to their least pessimistic since March.

As restrictions are gradually lifted, my latest forecasts (below) see economic activity recovering relatively quickly next year. Like the OBR’s ‘upside scenario’, GDP returns to pre-Covid levels by end-2021 and unemployment remains relatively low (perhaps peaking below 6%).

Crucially, there is no significant long-term scarring either to the economy or the public finances, other than a step increase in the level of debt (which is easily financed at very low interest rates). There is also no need for tax rises, penny-pinching, or dire warnings that ‘our economic emergency has only just begun’…

Well Said!!! Julian, you certainly bring some hope for us, rather than the doom and gloom from our Chancellor.

LikeLiked by 1 person

Great piece of work

LikeLike