The further contraction in the UK economy in October confirms that Budget speculation has killed growth, with GDP falling by 0.1% on both the single month and three month on three month comparisons. What’s more, the weakness was broad based (so not just the fallout from cyber attack at JLR). But this leaves some important questions to be answered.

1. How did we get here?

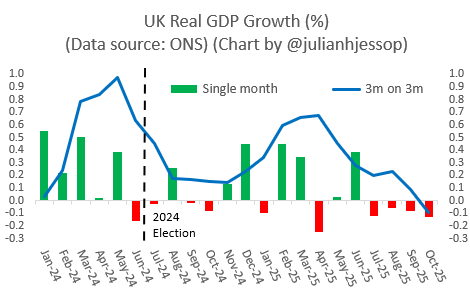

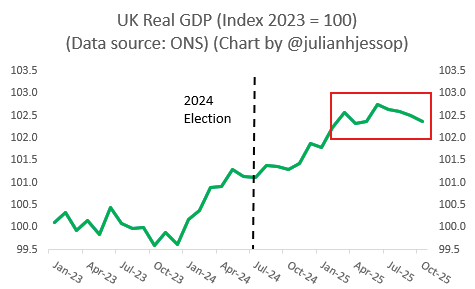

My first chart uses the detailed ONS data (to four decimal places!) rather than the rounded numbers. On this basis, the UK economy has now contracted for four months in a row. Indeed, GDP fell in 9 of the first 16 months of the Labour government (again, before taking account of some favourable rounding).

Here is the same data in levels terms. Labour inherited an economy that was growing strongly, albeit from a low base. However, the renewed burst of growth at the start of this year is now a distant memory.

The economy began to falter in the spring when the increases in employers National Insurance and other business costs in last year’s Budget finally kicked in.

There was then a brief recovery as fears of a global trade war faded, but this was followed by an extended period of uncertainty ahead of this year’s Budget. The leaks, unhelpful speculation and negative briefings clearly undermined confidence and activity across large parts of the economy.

2. What about November – and 2025 as a whole?

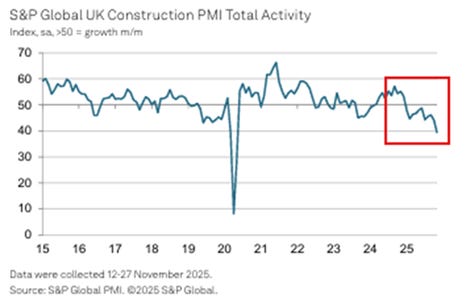

Worryingly, October is unlikely to be the low point. There was still nearly a full month of Budget uncertainty in November. The early survey evidence from a wide range of sectors suggests that activity fell again last month. The ongoing slump in construction is just one example (and a damning verdict on Labour’s ambitions to “build baby, build!”).

Even if GDP defies the odds and manages to stabilise in both November and December, the economy will have contracted by about 0.2% in the fourth quarter compared to the third. In turn this would put full-year growth at around 1.3%, meaning that the OBR’s upwardly-revised forecast of 1.5% made just last month is unlikely to be met.

3. So, is the economy in recession?

This depends on what you mean by ‘recession’!

The usual definition in the UK is two successive quarters of negative growth. On that basis the UK is not in recession, or at least not yet, because the economy grew by 0.1% in the third quarter. It is probably not there yet either in terms of GDP per head, which was flat in the third quarter.

Nonetheless, the UK economy is flirting with recession on other definitions. In particular, the UK may now be on the cusp of a significant decline in activity that is spread across the economy and lasts more than a few months, which is the usual definition of recession in the US.

Either way, though, the bigger picture is that this period will certainly feel like a recession to businesses struggling to stay afloat and to people worried about losing their jobs. And even if GDP growth is just the right side of zero, it will be far short of the numbers required to repair the public finances. That would probably require many years of growth nearer 2%.

4. What happens next?

The easing of uncertainty after the Budget might still allow a bounce in activity next spring. In contrast to 2024, most of the latest tax increases will not take effect for several years. It is therefore also still possible that any recession, however defined, will be a relatively shallow one by past standards.

Similarly, the combination of falling activity, high inflation and rising unemployment that the UK is experiencing now is still only ‘stagflation-lite’ compared to the full-fat version of the 1970s.

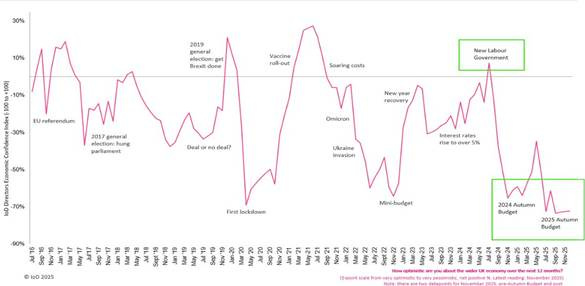

Nonetheless, it is very hard to restore economic confidence once it has been lost. The latest Institute of Directors Economic Confidence Index speaks for itself.

The government appears to have given up on growth in favour of policies aimed at redistributing income and increasing state intervention across the economy. This has undermined the incentives to work, save and invest, and squeezed any positivity out of the private sector.

5. How should the Bank of England respond?

The Bank of England is now almost certain to cut interest rates again next week, but only because the mounting weakness of the economy and especially the jobs market are offsetting worries about high inflation. This will be nothing to cheer.

For what it worth, I think the Bank should continue cutting rates but only gradually and should stop at 3.5%, which would be a neutral level. The MPC’s job is to worry about inflation, not to bail out a fiscally incontinent (and economically incompetent) government which has no growth strategy of its own.

Put another way, if the prospects for the UK economy really hinge on whether official interest rates are 4% or 3.75%, or even cut to 3%, we are truly doomed…