If you believe the media coverage of the latest consumer confidence surveys, household spending is set to collapse under the weight of the cost of living crisis, dragging the UK economy into a deep recession. But how reliable are these signals?

As always, it is worth digging past the headlines. The GfK measure of consumer confidence did indeed fall to a record low in May. But the detail showed that people were less pessimistic about their own finances than they were about the economy as a whole.

This distinction is crucial. It is no surprise that people are worried about the general economic situation: we are constantly being told that the country is going down the plughole. But when it comes to people’s own finances, things do not look quite as bad.

What’s more, the forward-looking components of the surveys are generally holding up better than the backward-looking ones. Sentiment towards personal finances over the next 12 months actually improved in May, albeit by just one point (see table below). This is not ‘free fall’.

The YouGov/Cebr Consumer Confidence Index, released earlier this month, is telling a similar story. The headlines focused on responses to the question “compared to one month ago, how has your household’s financial situation changed?”. The resulting index tanked to a new record low in April.

But this is not really telling us anything new. After all, April was the month when the energy price cap was lifted and National Insurance contributions went up. To be frank, I was more surprised this index was not even weaker.

Instead, the real value-added in the Cebr survey are questions on metrics like house prices and, most importantly, job security. These components are still pretty resilient (see table below). This means that households with savings built up during the pandemic are more likely to be willing to use them to prop up spending even as disposable incomes fall.

Consistent with this, UK retail sales volumes were better than expected in April, rebounding by 1.4%. Admittedly, this was led by strong growth in alcohol, confectionery and tobacco sales – possibly an Easter distortion, or people drowning their sorrows.

But it is also worth noting the strong growth in clothing sales. This fits in well with other evidence that life is finally getting back to normal after Covid, including a revival in the hospitality sector (not part of ‘retail’). People are getting ‘glammed up’ again for weddings and holidays, and socialising.

What about the often-repeated claim that large falls in consumer confidence are ‘always’ followed by recessions? In fact, the sentiment surveys are not that reliable.

For example, UK consumer confidence was relatively weak in the wake of the vote to leave the EU in 2016 (another example of people reflecting the gloomy headlines at the time). But the UK economy held up much better than many had feared – ‘despite Brexit’.

Another precedent was set in 2011, when both consumer confidence and real incomes fell sharply, but households were also willing to reduce their savings rates in order to maintain spending.

The upshot is that there are several reasons for optimism to offset the dire headlines. One is the continued strength of the labour market. Another is the large stock of savings built up during the pandemic.

There is also more support coming soon from the government, including the increase in the National Insurance threshold in July, which is a meaningful tax cut.

It is a similar picture in the United States. Consumer confidence has also fallen sharply. But the labour market has remained robust and the latest retail sales data have been more resilient than expected.

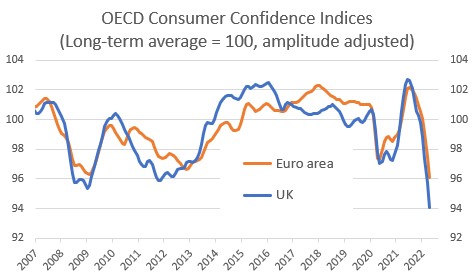

I would not pay too much attention either to the fact that the headline numbers for consumer confidence are a lot lower in the UK than in the euro area. UK consumers are almost always more negative than those elsewhere (notably in the GfK surveys). While confidence in the euro area is above its own record lows, it is not far off.

Of course, there is no room for complacency. The trend in UK retail sales is still downwards and confidence is clearly fragile. Unlike in other countries, consumers here have been hit by the double-whammy of soaring inflation and higher taxes. That also helps to explain why the UK has seen a bigger fall in confidence using the OECD indices, which adjust for some of the national biases (see chart below). The poorest households are also the least likely to have savings or other assets to fall back on.

Nonetheless, there is some reassurance to be found – if only people were willing to look for it. We know that bad news usually sells better than good news, and some commentators can barely conceal their glee at the chance to bash the government, or to run down the UK. Just don’t pay them too much attention.

This is an extended version of a piece first published by The Spectator on 20th May 2022