The lacklustre GDP data in May have put a significant dent in hopes of a rapid turnaround in the UK economy, but I’m not going to bin my relatively optimistic forecasts just yet. I still expect the shape of the recovery to look roughly like a ‘V’, with GDP back close to pre-Covid levels by the end of the year.

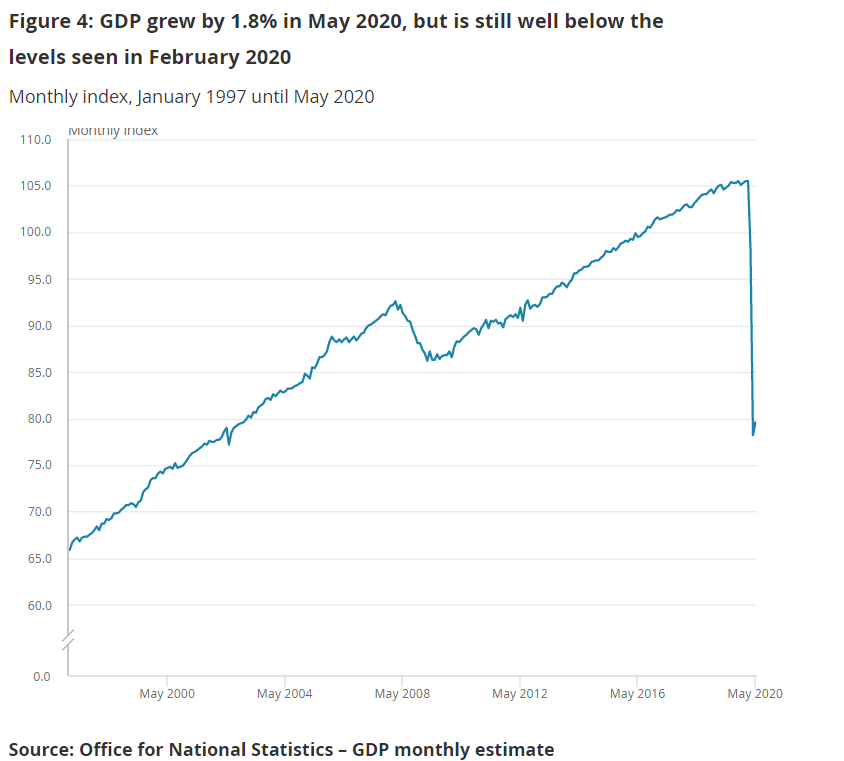

To be clear, the May numbers were disappointing. GDP picked up by just 1.8% m/m, compared to consensus forecasts for growth of 5% or more. This is pretty feeble given the extent of the decline in the previous two months – and it barely shows on the chart below. Nonetheless, there are three good reasons not to panic.

First, monthly GDP data are relatively unreliable at the best of times, and especially now. In the words of the ONS, ‘GDP estimates for May 2020 are subject to more uncertainty than usual as a result of the challenges we faced in collecting the data under government imposed public health restrictions’.

Second, economic activity itself was still being heavily constrained by these restrictions. One way to quantify the lockdown is to look at the Government Response Stringency Index, compiled by researchers at Oxford University, which is a composite measure based on nine indicators including school closures, workplace closures, and travel bans.

The key point here is that other major European countries have been quicker to relax their restrictions. This has been reflected in a faster economic recovery too; for example, industrial production in the euro area rose by 12.4% m/m in May (compared to 6% in the UK), with retail sales up by 17.8% (12.0%). Hopefully, those of us still expecting a (roughly) V-shaped recovery in the UK will only have to wait a month or two longer for some much better GDP numbers as well.

Third, we are now in mid-July, so the May GDP numbers are already two months old. More timely UK data are reassuring. In particular, the main weak spot in May was the services sector, where output rose by just 0.9%. The pick-up in retail in May was offset by falls in other categories such as ‘professional, scientific and technical activities’, and ‘information and communication’. This suggests that while consumers are starting to spend again, businesses are lagging behind. However, the services PMI, which was still just 29.0 in May, has since rebounded to 47.1 in June.

We also already have further evidence of recovery in the consumer sector. The BRC Retail Sales Monitor reported that sales were 3.4% higher in June than the same month last year. And while footfall is still well below year-ago levels, consumers do appear to be spending more on each visit to the shops – or online. Consistent with this, Visa’s UK Consumer Spending Index (CSI) has reported much smaller annual declines and a record 16.6% m/m increase in June, despite an abundance of caution.

Of course, the crucial uncertainties remain, including the risks of a second wave of coronavirus or a surge in job losses as government support is withdrawn. I will write more on these issues shortly (as well as how to interpret the PMIs).

For now, the main message is simply that May’s weak GDP data are not a gamechanger. The recovery is still likely to surprise on the upside over the remainder of the year as the official lockdown is eased further, and as both consumers and businesses feel more confident about spending again.

I think a rapid recovery was always a pipe dream but I do agree with your optimism. Losing cashflow has hit many businesses hard, resulting in a recovery process that’s slower than the shutdown – a little like trying to bring a heavy vehicle back up to speed after it’s stopped. I’m also expecting to see a change in the type of businesses due to a forced creative destruction. Some will fold, others will take their place, market dependent. And it’s certainly great to see higher sales figures overall, although I wonder how much these are affected by higher prices in certain areas? My food bill certainly went up, although I – consciously – wasn’t buying any more than usual. Job losses and another coronavirus wave are definitely concerns, so I look forward to reading your upcoming posts on these!

LikeLiked by 1 person

Thanks Rachael – all good points. The BRC and Visa card spending data are in cash terms so might have been flattered by rising prices. However, the inflation data have been weak, and we also have other data that are in volume terms and have been good too. The official retail sales data out tomorrow (24th) are in volume terms and will hopefully confirm this. PS. I’m writing something for Sunday Telegraph on the labour market and will post here too.

LikeLike