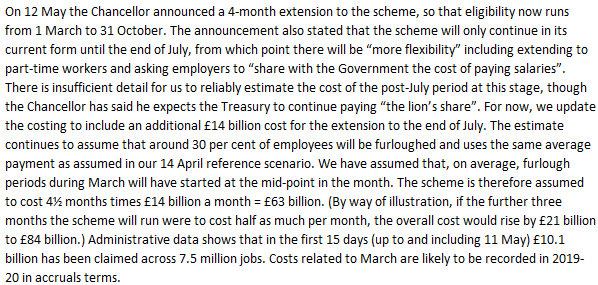

The economic data for April were bound to be awful and those for the public finances were no exception. Government borrowing last month alone (a record £62.1 billion) was almost as large as the deficit in the whole of last year (£62.7 billion). This included £14 billion for the first full month of the coronavirus job retention scheme. How long can we keep this going? And how do we wean ourselves off this extraordinary level of state subsidy, before it is too late?

For now, it is right not to panic about the budget deficit itself. There is a huge difference between a temporary increase in borrowing in response to a one-off shock, like coronavirus, and a longer lasting or structural deterioration in the public finances.

In the case of the former, we should simply take the hit on annual borrowing, even if this year’s deficit turns out to be as large as the Office for Budget Responsibility’s latest estimate of £298 billion. We should also accept that debt will jump to well over 100% of national income. Low interest rates will keep servicing costs down and the burden of this debt, measured as a share of GDP, will still fall over time as the economy recovers.

So far, not so bad. Indeed there are some good reasons for optimism about the prospects both for the economy and the public finances. As I have written here before, activity has already begun to pick up again, the government’s hugely expensive measures have at least protected the great majority of businesses and jobs, and the UK’s relatively dynamic economy and labour markets should soon be able to replace any that might be lost.

Nonetheless, there is still plenty that could go wrong. For a start, the longer the economy is kept shuttered, the greater the risk of permanent scarring. This is what the Treasury appeared to have assumed in the alternative fiscal scenarios which were reported in the Daily Telegraph earlier this month. This would then be the time when more difficult decisions need to be made about public spending and taxation.

At least as importantly, there is a danger that a narrow focus on the fiscal implications of high levels of state intervention will distract us from the broader economic costs. The coronavirus job retention scheme (CJRS) is a prime example of this.

Initially, it made sense for the state to subsidise payrolls in order to avoid the need for good businesses to lay off and then rehire workers when the economy reboots, with all the costs and uncertainties that would bring both for employers and employees. It also made sense that the scheme encouraged firms to concentrate any work among a small number of full-time employees and furlough the rest, given the importance of keeping as many people at home as possible. Now, though, the balance of risks is shifting.

This requires a shift in the mindset too. When he announced the extension of the CJRS on 12th May, the Chancellor said that ‘nobody on this furlough scheme wants to be on this scheme… it’s not their fault that their business has been asked to close’. The sentiment was entirely understandable, but it would have been good to see an acknowledgement of the adverse impact on incentives if some people are paid 80% of their normal income not to work, or to change job, or set up a new business.

The CJRS also provides a free option for existing firms to keep workers on their books, at mounting cost to the taxpayer, even if it would actually make more sense for them to be redeployed elsewhere. No wonder the scheme is so popular both with trade unions and business lobbies.

To be fair, the Chancellor clearly recognises these risks. The scheme may have been extended until the end of October, with furloughed employees still expected to receive a generous 80% of their normal salary, but there will be at least some changes from August. In particular, furloughed employees will be able to return to work part-time, and employers will be required to contribute towards the costs of the scheme.

In summary, a temporary increase in borrowing is a price worth paying to save lives and protect businesses and jobs in these extraordinary times. But if it continues much longer, this huge amount of state intervention will simply distort the economy, undermine market incentives, and ultimately hold back the recovery. A bolder plan to scale back the CJRS would be an excellent place to begin.

This article first appeared in the Daily Telegraph (online)

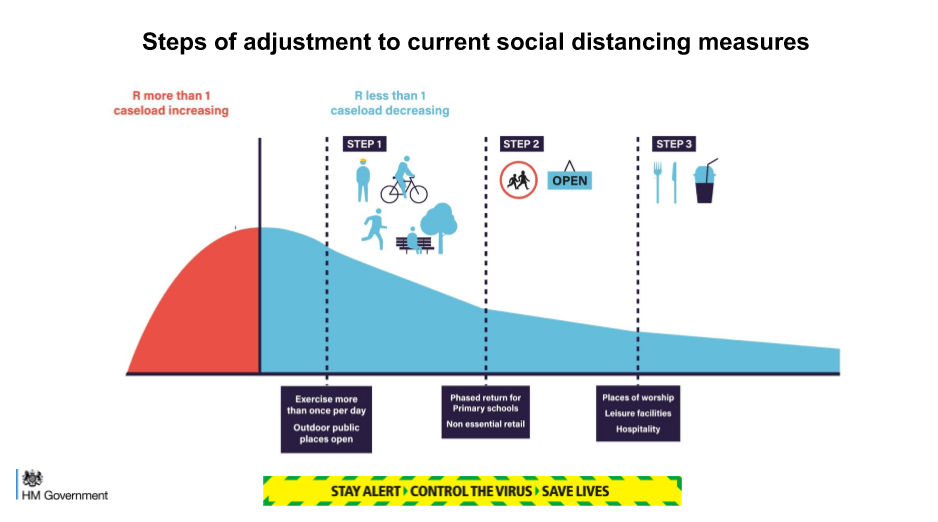

PS. on Saturday 23rd The Times reported that, from August, firms using the CJRS will have to pay 20-30% of wages of furloughed workers and their employer NICs. I’d strongly support these changes. The Times also reported that employer contributions will be required in all sectors, including any still in lockdown. But we now know that non-essential retail will be allowed to re-open in June (part of ‘step 2’ of the lifting of restrictions) and its reasonable to expect leisure and hospitality to be open by August (part 3). Even if not, there shouldn’t be much longer to wait.

PPS. The OBR’s latest guess at the budget deficit for 2020/21 (£298 billion) only allows for the cost of the CJRS until the end of July (as they explain below). Assuming the monthly costs of the CJRS are halved from August to October, you’d still have to add £21 billion. At face value that would take this year’s deficit well over £300 billion. But I still think it will come in lower than that, both because the initial hit to GDP won’t be as large as the OBR assumed and because the lockdown will (hopefully) be lifted sooner.