In the early stages of the Iran crisis the markets priced in a relatively benign scenario. The conflict was expected to be short, lasting days if not weeks, with limited fallout for energy prices and for the global economy. A month on, this has proved to be far too optimistic.

Indeed, the future looks increasingly binary. Either President Trump steps back from the brink within a couple of weeks, or the crisis escalates beyond any one person’s control, dragging the world into recession.

For what it’s worth, I still think the former is far more likely. This is the TACO playbook (“Trump Always Chickens Out”), which we have seen several times before during the (rather less apocalyptic) tariff wars.

Clearly, the Iran war has not worked out as the US hawks had hoped, and it has landed badly at home too. The US economy is not immune to higher energy costs and the President’s popularity is already sinking. More US military casualties could be the final straw.

The President has already started to prepare an “off ramp” by declaring that the US and Israel have now achieved “regime change” in Iran, by killing at least one layer of leadership, even though the hardline IRGC actually seems to have strengthened its grip on the country.

The other stated war objective was to prevent Iran from developing nuclear weapons. Given that the White House had already claimed last June that “Iran’s Nuclear Facilities Have Been Obliterated”, it would not be a huge leap to insist that this objective has now been achieved too.

In this “TACO” scenario, markets could recover quickly. Unfortunately, some economic damage has already been done, especially in Europe.

The flash estimate suggests that euro area inflation jumped from 1.9% to 2.5% in March, entirely due to higher energy costs. The equivalent UK CPI is not due until 22 April, but it will jump too, probably from 3.0% to around 3.5%.

Business and consumer confidence have also weakened. The flash UK PMI Composite Output Index fell to a 6-month low of 51.0 in March. The grim detail included the biggest monthly jump in manufacturing input cost inflation since sterling was ejected from the ERM in 1992.

But even at this stage, recession is not yet inevitable.

The recent surge in natural gas prices is still nowhere near as large as that in 2022, when Liz Truss introduced the Energy Price Guarantee (EPG). Some much more limited and targeted support could be the most that is required now – if any is necessary at all.

Admittedly, Cornwall Insight’s latest forecast is for a rise of £288 (or 18%) in the Ofgem cap on domestic energy bills in July, compared to the April level of £1,641. But this is actually slightly less than their previous projection, and usage is lower in the summer anyway.

It is also worth stressing that we are only about halfway through the “observation window” for wholesale costs for the July cap, which closes on 18 May. A lot could therefore still change, in both directions.

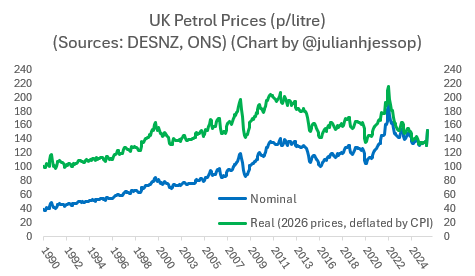

In the meantime, while it may not be a popular thing to say, petrol prices are still not particularly high in real terms, and a further small increase may be the least bad way to manage demand in the face of a supply shock.

Much will depend too on the Bank of England. My best guess is that the Bank will keep interest rates on hold, which should provide at least some relief to those who are now fearing a series of rate increases. The MPC needs to talk tough on inflation sometimes to maintain credibility, but it is far from certain that it will follow through.

Rate rises would not, of course, cap the upward pressures from the prices of energy and other commodities. The only reason to hike would be to limit the second round effects, notably on inflation expectations and on wages. However, the fragility of demand and the weakness of the labour market should do that anyway.

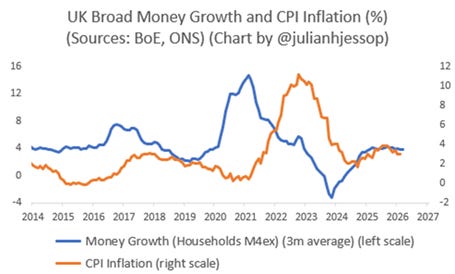

Another big different from 2022 is that growth in the money supply has been relatively subdued, which makes it much less likely that inflation will rise as far, or for as long.

Finally, at least five of the nine MPC members would have to vote for a hike, which sets a high bar. It is not so long ago that all nine were voting for cuts or had a clear bias towards further easing.

On balance, then, my usual advice not to panic still applies. But the “Trumpageddon” scenario does need to be taken seriously.

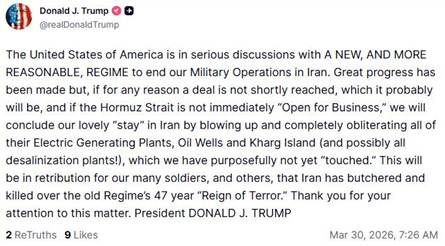

For a start, the President has evidently lost the plot. Just read the following post and remember that deliberately targeting civilian infrastructure – such as water supply – is generally considered a “bad thing”. Perhaps he is bluffing (“The Art of the Deal”). But who knows?

It is not difficult to imagine a new scenario where the crisis persists and actually spreads beyond the Strait of Hormuz, with Iranian proxies in Yemen opening a second front that also leads to the closure of the passage for many other goods through the Red Sea.

A plausible “worst case scenario” could therefore see oil at $200 per barrel combined with Covid-like disruption to supply chains more widely. This would trigger a global recession, with the UK hit especially hard.

This is not the place to look for investment recommendations and what follows is not intended as such. But the conventional “safe haven” of government bonds would still struggle in this scenario, given the inflation risks and the costs of energy bailouts. Even gold might struggle as investors look to take more profits to cover losses elsewhere.

A long position in oil would be the obvious hedge, with overweights in cash and perhaps in the Japanese yen helping to limit the downside.

To repeat though, “Trumpageddon” should still be avoided, if only because the President himself would not be daft enough to unleash it.

Would he?

ps. you can follow me on X (formerly Twitter) @julianhjessop and on BlueSky. I also post regularly on Substack.