Rachel Reeves is getting her excuses in early ahead of next month’s Budget, which looks set to be a painful repeat of last October’s “one off”.

The Chancellor has already blamed “external headwinds”, “Tory austerity” and “the ongoing impact of Liz Truss’s mini-Budget”. It is no surprise that she has now dropped the “B-word” too.

Speaking to Sky News last week, the Chancellor said “already, people thought that the UK economy would be 4% smaller because of Brexit”, adding that “there is no doubting that the impact of Brexit is severe and long-lasting”.

The “4%” refers of course to the Office for Budget Responsibility’s assumption that Brexit will eventually reduce UK productivity by 4% compared to staying in the EU.

The OBR is continuing to respect pre-Budget “purdah”. But Treasury officials – and even Rachel Reeves herself – are already briefing that the expected downgrade of the productivity forecasts will partly reflect a more pessimistic assessment of the impact of leaving the EU.

A downward revision of just 0.1-0.2 percentage points to the annual growth forecasts could add another £10-20 billion to the “black hole” in the Budget, prompting even bigger tax increases.

But this ‘Brexit blame game’ is pretty desperate stuff.

For a start, the OBR’s original 4% is built on some remarkably shaky foundations.

The 4% figure itself was simply a crude average of the results of 13 external studies. These studies were all done before the final shape of the exit agreement was known, They also used a variety of different models and assumptions, most of which now look far too pessimistic.

Moreover, the OBR’s take on the 4% relies on an implausibly large hit via the trade channel. Most economists would agree that an increase in barriers to trade is a ‘bad thing’. That is just basic economics – and firmly in the Classical Liberal / ‘free markets’ tradition. But while the theory is sound, the numbers fail a basic “sniff test”.

The OBR assumes that the new frictions to trade with the EU are so severe that they will permanently reduce total UK imports and exports – both goods and services – by as much as 15%. The resulting fall in the “trade intensity” of the UK economy is then assumed to cause a 4% reduction in productivity, with the full impact felt after 15 years.

These strong assumptions are only weakly supported by the actual data – if at all. The UK’s exports of goods have underperformed relative to our peers, at least in volume terms, but by far less than many feared. More importantly, overall trade has held up much better than expected, partly due to the continued strength of services.

At most, the UK’s “trade intensity” might be a few percentage points lower than it would otherwise have been. This is unlikely to have any significant impact on productivity in a large, advanced economy which will remain relatively open.

But even if you take the OBR’s assumption of a 4% long-term hit to productivity at face value, it is nothing new. Indeed, it dates back to the March 2020 EFO, and the underlying assumptions about the impact on exports and imports first appeared in the November 2016 EFO. So how can it explain the expected downgrade in next month’s Budget?

One answer might be the OBR is simply feeding more of the long-term hit into the medium-term forecasts. The full impact of the 4% hit was spread over 15 years, so about 0.25% per year. In the March 2020 EFO, the OBR assumed that around one-third of the hit had already happened and that one third was still to come in the following five years – taking us to 2025. Perhaps the remaining one-third will be baked in next month.

But that explanation is just speculation on my part. It certainly would not mean that the long-term impact is any worse than previously thought.

Another possible answer is that the OBR has decided that the initial impact of Brexit was more severe than anticipated, so that it takes longer for actual productivity to return to its trend rate.

Admittedly, some studies have suggested that the UK economy may already be as much as 5% smaller than if we had remained in the EU. These studies typically attempted to quantify the impact that Brexit has had to date by comparing the actual performance of the UK economy with those of similar countries.

Most famously, economists at Bloomberg claimed in 2023 that the UK economy was already about 4% smaller, then costing the UK about £100 billion a year in lost output (and about £40 billion in lost revenue). This was mostly done by comparing how the UK has performed relative to the rest of the G7.

The most sophisticated of these studies (notably work by the CER) rely on a computer algorithm to select a weighted combination of economies whose performance best matched that of the UK before Brexit. The actual performance of the UK economy since Brexit is then compared to this control group, or ‘doppelganger’, and the difference taken as a proxy for the impact of leaving the EU.

But all these studies are fundamentally flawed, because they rely on the assumption that any divergence in the UK’s economic performance can only be due to Brexit. This is clearly nonsense.

Among other things, this approach glosses over the impact of other shocks, notably the pandemic and the global energy crisis, which are bound to have affected different economies in different ways. It also ignores any other national factors, including different policy choices on energy policy, the labour market, tax and regulation.

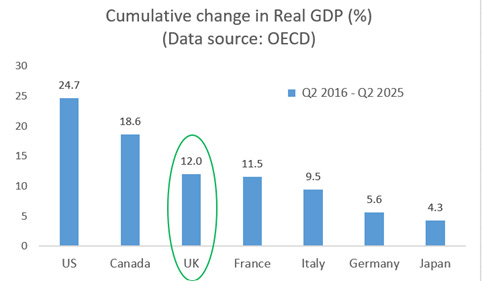

In any case, looking simply at headline GDP, the UK has outpaced Italy, France and Germany since 2016. Even in terms of output per head, “Brexit Britain” is continuing to track midway between France and Germany. We are certainly not an outlier.

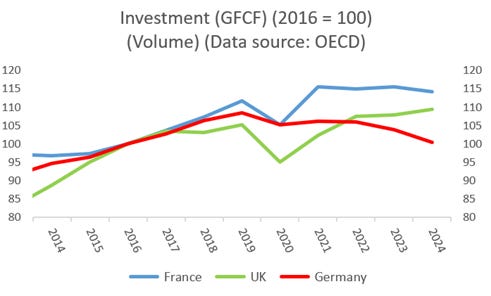

Treasury officials have also suggested that the initial hits via trade and investment have been worse than expected. But again there is little to support this claim. In particular, UK business investment is clearly recovering as uncertainty eases.

The timing would also be very odd. The 4% figure was based on the expected terms of the exit from the EU back in 2016. As such, it does not take account of the actual deal, which was relatively liberal, or any changes since then, including any benefits from Labour’s “reset” and from the new trade deals with other countries.

Rachel Reeves herself argued in her Sky News interview that – “now, of course, we are undoing some of that damage by the deal that we did with the EU earlier this year on food and farming, goods moving between us and the continent, on energy and electricity trading, on an ambitious youth mobility scheme”.

She has also been careful (at times) to blame the “way in which we left the EU”, rather than Brexit itself.

Even Bank of England Governor Andrew Bailey’s recent remarks would not justify a more pessimistic view. He said that he expects Brexit’s impact on economic growth to be negative “for the foreseeable future”. That has been the Bank line for many years and is nothing new.

But he then said that “over a longer time there should be a positive, albeit partial, counterbalance” as trade adjusts. In fact, he suggested this may already be happening. In other words, the drag on growth will fade over time.

Logically, then, the OBR should now be less pessimistic about the long-term impact of Brexit, not more. A further downgrade now would be a damning verdict on the Labour government’s efforts to improve the terms of the UK’s departure from the EU.

Instead, the more straightforward explanation is simply that the OBR has decided to put more weight on the UK’s dismal productivity performance ever since the Global Financial Crisis in 2008.

In short, the evidence that Brexit has been a key factor here is thin. But even if you do buy into the OBR’s 4%, it is not clear why this would justify a further downgrade now.

This is an extended version of a piece first published by CapX on 21 October 2025

You can follow me on X (formerly Twitter) @julianhjessop and BlueSky @julianhjessop.bsky.social

I also post regularly on Substack at https://substack.com/@julianhjessop