Speculation that Liz Truss is about to make to return to frontline politics has prompted a flurry of dodgy claims and daft statistics about the economic cost of last September’s mini-Budget. Here’s a quick debunking of the most common.

I’ll start with the biggest number: £74 billion (sometimes cited as £73 billion).

This appears to have been lifted from a headline in the Daily Express (26th October) which claimed that ‘Kwasi Kwarteng’s budget blunder cost UK an eye-watering £74 billion, finance chief reveals’.

Digging deeper, this was the Debt Management Office (DMO’s) estimate of the increase in the Net Financing Requirement for the fiscal year 2022-23 between April and September (actually £72.4 billion, but near enough).

This figure was included in the Growth Plan published on 23rd September, so was not news. In short, this was the extra money that the DMO expected to have to raise from the bond markets in 2022-23, relative to the projections in April.

Crucially, most of this figure was accounted for by the additional government support to help people and businesses with their energy bills. It also included the reversal of the 1.25 percentage point hikes in National Insurance contributions for both employees and employers.

It is therefore misleading to describe the ‘£74 billion’ (or whatever) as a cost to the UK. The implication is that the UK is somehow ‘£74 billion’ worse off as a result of policies adopted to prevent an energy crisis from becoming a catastrophe. This is clearly nonsense. I wonder also if those gleefully still retweeting this are happy to rely on one iffy headline in the Express!

There is another only slightly smaller number doing the rounds: £65 billion.

This is the notional amount that the Bank of England said it was willing to commit to buy UK government bonds (aka ‘gilts’) to stabilise the market in the wake of the mini-Budget.

To recap, the rise in gilt yields was exacerbated by the increased use of liability-driven investment (LDI) strategies by some pension funds. This triggered a vicious spiral of margin calls and forced gilt sales, driving up yields further. The Bank of England (and other regulators) should have been on top of this much earlier.

In the event, though, the Bank ‘only’ spent about £19 billion, on which it actually made a profit of about £4 billion. Claims that the mini-Budget ‘wiped £65 billion off the British economy in a month’ are therefore nonsense too.

The third ‘zombie statistic’ is the smallest: £30 billion.

This one appears to be based on a report in the Observer (12th November) which claimed that ‘Liz Truss’s disastrous mini-budget cost the country a staggering £30 billion’.

The £30 billion figure came from (old) analysis by the Resolution Foundation (RF).

Around £20 billion of the £30 billion was simply a (high) estimate of the cost to the Treasury of those tax cuts in the mini-budget that have survived. This is mainly accounted for by the reversal of the increases in National Insurance (NI) contributions, and partly by the reductions in Stamp Duty.

Ironically, these measures were widely welcomed at the time, in part because they made a deep recession less likely. It is certainly odd to characterise £20 billion of tax cuts as a cost to taxpayers!

The remaining £10 billion was an (old) RF estimate of the annual increase in the government’s cost of borrowing that might be attributed to the fallout from the Truss premiership. This is just speculation. Indeed, most market commentors would agree with me that any significant risk premia in UK assets have long since evaporated.

Of course, some will argue that even if the £74/65/30 billion figures are wrong, the mini-Budget ‘wrecked the economy’ (it didn’t) and that we are still paying the price now (we aren’t).

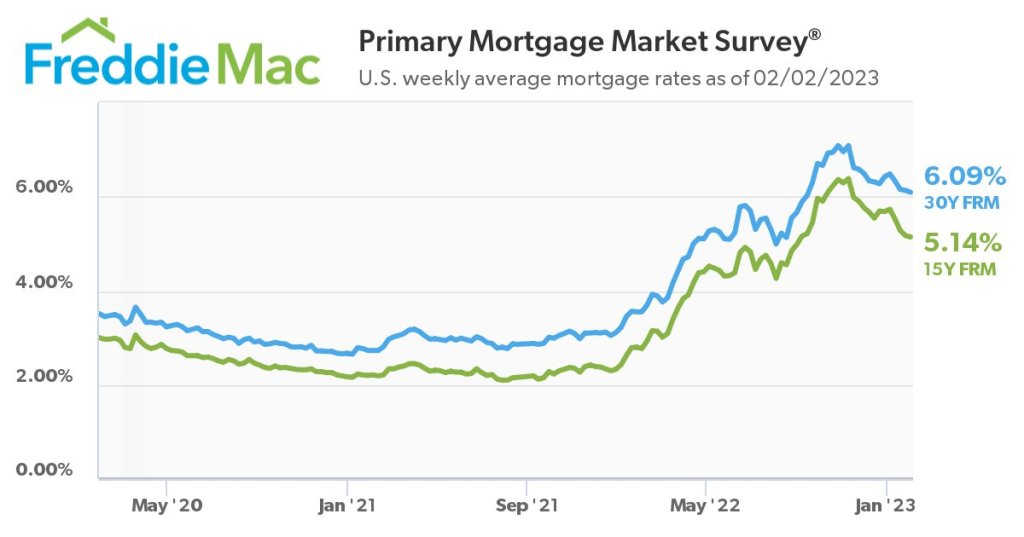

One example of this dubious narrative is the many tweets which blame the mini-Budget for the sustained increase in mortgage interest rates. But mortgage rates (and mortgage spreads) have also surged in many other countries, notably the US.

Another is the attempt to pin the IMF’s recent downgrade of the UK’s growth forecast for 2023 on ‘the country’s disastrous autumn of Trussonomics, which came too late for the IMF’s October forecasts’. This interpretation makes little sense.

In its October World Economic Outlook, the IMF itself noted that the fiscal expansion in the mini-Budget was ‘expected to lift growth somewhat above the forecast in the near term’, albeit at the cost of complicating the fight against inflation.

The new factor is therefore that Jeremy Hunt has tightened fiscal policy and signalled that the government will scale back its help with energy bills. This is a rather better explanation of why the IMF has downgraded its UK forecast for 2023.

In contrast, the forecasts for the euro area have been nudged up slightly, reflecting the announcements of additional fiscal support in the form of energy price caps and cash transfers.

Here, critics may respond that the reversal of policy in the UK was necessary to restore credibility in the financial markets after the botched implementation of Trussonomics, and that interest rates are still higher than they would otherwise have been.

But there is actually very little evidence to support this. In any event, it should have been sufficient for a new Chancellor to cancel the surprise measures that most unsettled investors – notably the additional cuts in personal taxes. Instead, the pendulum appears to have swung too far the other way.

History is often written by the victors. However, it is utterly bizarre to blame a forecast revision which is mainly due to tighter fiscal policy and expectations of still-high energy prices on a plan to cut taxes and provide more support with energy bills!

Helpful clarifications which should be more widely understood. But the misrepresentations too entrenched so a lost cause and the narrative has moved on.

Useful if PSE could offer an alternative policy prospectus pre-empting the Budget and a yardstick for judging how it will grow national income per head with by tax cuts freeing up the supply side as being anti-inflationary eg. deep cut in “effective” corporation tax rate to encourage investment including training and R&D, cutting SDLT very sharply across the board to get transactions and new house-building moving (raising associated consumer goods demand), removing penal landlord taxation (dwellings available dropping sharply but each one commonly accommodates several people so multiplying up the shortage and raising rents more given that purchase is even more difficult given the general housing shortage ), cut CGT to encourage more capital transactions and investment and so on. Cutting marginal taxes, pension penalties, benefits anomalies to incentivise the economically inactive. And so on ie. not not unfunded demand side taxes when capacity is constrained. And so on. Student loan relief – interest rates cut etc. Dare one suggest that given the elasticites there could be an increase in net tax take in short order….

Increased labour supply plus investment driven productivity growth will reduce inflation and raise NI/head pretty quickly in a virtuos cyclical pick up circle as history shows. Personal tax cuts become viable later but the current “gas windfall” (also predicted by PSE) should not be used on these at this juncture/

Do nothing and we get nothing but decline.

LikeLike

Yep, that’s the way it was. Pity so many people don’t get it.

LikeLike