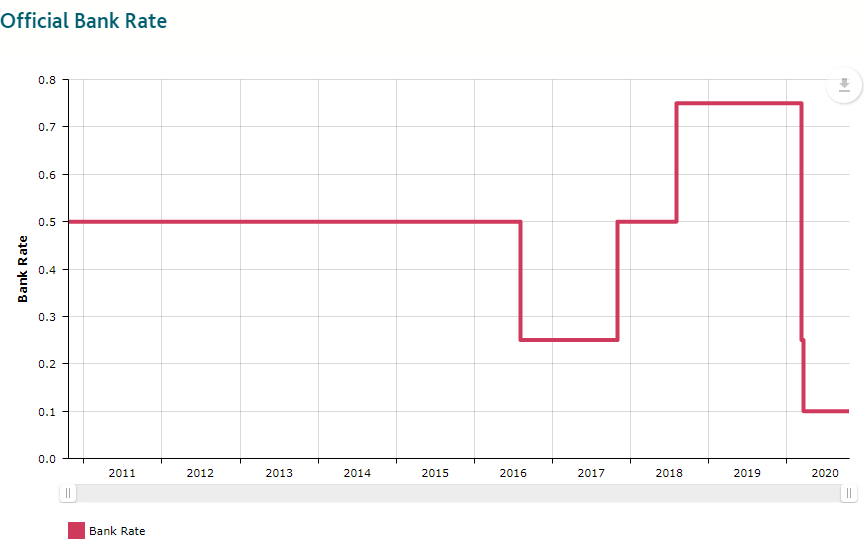

It’s hard to add much to the debate over whether or not the Bank of England (BoE) should cut its key interest rate, currently just 0.1%, below zero. The case against negative interest rates has been well made by David Smith, Liam Halligan and Peter Warburton, among many others, including MPC veterans such as Andrew Sentance. But the balance of costs and benefits might still depend on exactly which ‘interest rate’ we are talking about.

In particular, it might help to distinguish between deposit rates (i.e. what banks pay on money held with them) and lending rates (i.e. what banks charge for borrowing from them).

The BoE’s key interest rate – the ‘Bank Rate’ – serves both purposes. It is the rate that the BoE pays to commercial banks that deposit money at the central bank. But the Bank Rate also sets a floor for the rate that the BoE itself charges for borrowing, including the snappily-named ‘Term Funding Scheme with additional incentives for SMEs (TFSME)’.

The case for setting an official deposit rate below zero is arguably the weakest. This is most likely to damage the profits of commercial banks, because they will be reluctant to charge their own customers for making deposits. (This is discussed further in a recent talk by the MPC’s Dave Ramsden, who clearly favours more QE as the tool of choice.)

A negative deposit rate is also most likely to damage confidence more generally, not least among savers. And there is only so far below zero that you can set a deposit rate anyway, given the alternative of simply holding cash (paying 0%).

But the case for setting a negative lending rate may be stronger. Of course, deposit rates normally set a floor for lending rates, whatever their level. Suppose instead that deposit rates were 0.5% and lending rates were 0.25%. A commercial bank could then make ‘free money’ simply by borrowing at 0.25% and parking the proceeds back at the BoE at 0.5%.

However, it is possible to get round this by attaching conditions to lending at lower rates. This is what the ECB has done with its ‘Targeted longer-term refinancing operations’ (TLTROs), which charge an interest rate as much as 0.5% below the ECB’s deposit rate, which itself is currently minus 0.5%.

To qualify, participating banks’ lending need to meet certain criteria. In short, ‘the more loans participating banks issue to non-financial corporations and households (except loans to households for house purchases), the more attractive the interest rate on their TLTRO III borrowings becomes.’

In effect, the ECB is independently targeting lending rates and deposit rates – as discussed further here by Eric Lonergan and Megan Greene. They quote the ECB’s chief economist, Philip Lane, who wrote in March that ‘banks can borrow at the most favourable rates we have ever offered, provided that they continue to do their job of extending credit to the private sector. An important innovation is that, by setting the minimum borrowing rate at 25 basis points [now 50 basis points] below the average interest rate on the deposit facility, we are effectively lowering the funding costs in the economy without a generalised reduction in the main traditional policy rates.‘

In principle, then, the BoE could leave Bank Rate at 0.1% and lower the minimum interest rate on its equivalent TFSME scheme to, say, minus 0.5%.

To be clear, I would still not be keen on this. Another MPC member, Gertjan Vlieghe, seems a bit more enthusiastic about negative interest rates in general. But even he has suggested that this move would have to meet three tests: ‘it must be feasible, effective and appropriate’. Let’s run with these…

The first test refers to the ‘financial system being able to cope, operationally, with negative rates.’

There are precedents elsewhere for negative rates:

i) some Swiss banks charge a fee for taking large deposits;

ii) there are some mortgage products in Scandinavia where interest rates are effectively negative: borrowers still have to make regular interest payments but these payments, plus a bit more, are then deducted from the capital owed;

iii) the yields on many government bonds (including short-dated gilts) are also negative: holders still receive regular interest payments, but these are more than offset by the fact that they receive less back when the bond matures than they originally paid.

Nonetheless, negative rates are more likely to be ‘feasible’ in wholesale markets (where banks and other financial institutions deal with each other) than in retail markets (where banks deal with businesses and households). This is partly because financial institutions are more likely to be familiar with negative interest rates, especially if they are dealing in other markets where some rates are already negative.

It should also be easier in the case of lending rates than deposit rates, especially given the practical and presentational problems of charging ordinary savers for taking their money.

Vlieghe’s second test ‘refers to the benefits of negative rates outweighing the costs by a sufficient margin, i.e. negative rates should not be counterproductive to the aims of monetary policy’. This is arguably trickier, but again may be less of a problem for lending rates than deposit rates.

Vlieghe’s third test of appropriateness ‘refers to the economy actually requiring more monetary stimulus in order to meet the inflation target’. Even if the first two hurdles could be cleared, this would be my biggest problem with negative rates – or additional monetary stimulus of any kind.

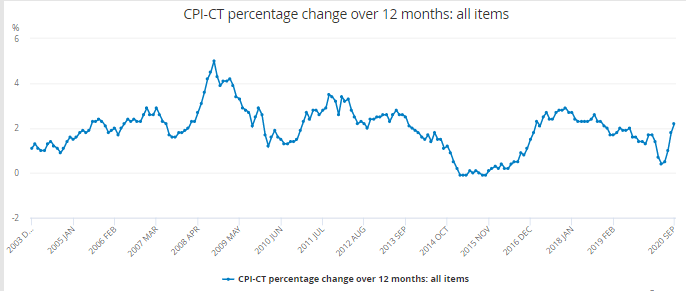

There is already speculation that the Bank of England will announce even more QE at its meeting in November, in response to the increased downside risks to the economy. In my view, this would be a mistake: consumer price inflation (CPI-CT, which excludes the temporary effect of tax changes) is 2.2%, inflation expectations are at a multi-year high and rising, and the broad money supply is booming.

Instead, the onus should be on fiscal policy to respond. Of course, monetary policy sometimes needs to support fiscal policy, but the Bank of England’s main job is to manage inflation, and there is already more than enough monetary stimulus in place to keep borrowing costs down.

In short, I can see how a new structure of interest rates could be designed to minimise the costs of going negative – essentially by cutting the cost of borrowing while leaving deposit rates where they are. Nonetheless, this would still seem to be far more trouble than it’s worth.

BoE should cut rates and keep it below zero. People will invest money instead of keeping it in savings account.

LikeLike