“Buy British, Goldman Sachs tells clients“. I had mixed feelings on reading this headline. It’s reassuring that the City is waking up to the prospect of an upturn in the economy next year. Goldman is surely right that clarity on the terms of the UK’s departure from the EU should emerge sooner under a Conservative majority government. However, the City’s forecasting record is pretty dire, particularly when it comes to Brexit. Ever since the referendum, forecasters have predicted a range of baleful scenarios which have notably failed to materialise. Here are five examples.

“A vote to leave the EU would immediately cripple the UK economy”

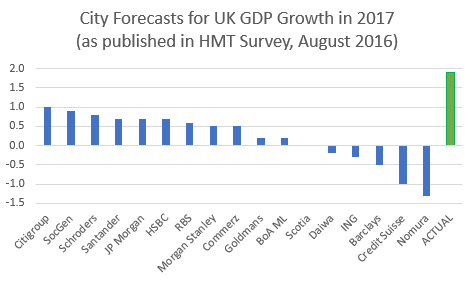

First, most City forecasters wrongly predicted that the leave vote alone would be enough to cause a sharp economic downturn. According to the monthly survey compiled by the Treasury, City forecasts made shortly after the 2016 referendum ranged from growth of just 1.0 per cent in 2017 to a contraction of 1.3 per cent, with many investment banks predicting an outright recession. In reality, the UK economy grew by nearly 2 per cent that year.

Some have found plenty of excuses for this failure, including the delay before Article 50 was triggered, the additional support provided by the Bank of England, and stronger growth in the rest of the world. But good forecasting is all about making allowances for these sorts of factors. (An honourable mention therefore to my old shop, Capital Economics, which predicted growth of 1.5 per cent in 2017.)

“Markets would remain in turmoil”

Second, the City was wrong on the market reaction too. Currency traders were caught out by the referendum result, prompting a sharp fall in the pound. There had at least been a consensus that sterling would dive in the event of a vote to leave, which was just about the only thing that the Treasury’s now infamous pre-referendum analysis got right.

But rather than this being followed by a sustained fall in equity, bond and property prices, other markets soon stabilised. Indeed, the fall in the pound actually helped, by boosting the sterling value of overseas earnings and maintaining the attractiveness of UK assets to foreign investors, albeit at the significant cost of higher import prices and a squeeze on real wages.

“Britain will lag far behind the rest of Europe”

This excessive pessimism about the impact of Brexit has continued ever since. The consensus is that the UK economy has already substantially under-performed as a result of the vote to leave. There is little doubt that output has grown more slowly than it would otherwise have done, mainly due to the jump in inflation and the impact of Brexit uncertainty on investment. But the gap is much less than many would have us believe.

In particular, the figures tossed around in the City, and elsewhere, are usually distorted by comparisons with the US, which has benefited from a large fiscal boost. The differences between the performances of the UK economy and our peers in Europe are much narrower. Indeed, the UK has kept pace with Germany since the EU referendum, even though the German model is often held up as a paragon for the UK to copy.

“Brexit will spark a mass exodus of City jobs”

Fourth, many City institutions have been wrong about the impact of Brexit on jobs in their own sector, let alone the economy as a whole. We were warned of a mass exodus even before the UK has actually left the EU. The reality has been very different.

A survey by the New Financial thinktank has identified more than 330 City firms which have already moved or are moving business, staff, assets or legal entities from the UK to the EU. Nonetheless, the actual number of jobs involved has been little more than trickle, partly offset by a reverse Brexit effect as firms from elsewhere have moved business here.

Of course, this could still change if the UK fails to secure a good long-term deal with the EU, but the UK’s strengths here are largely Brexit-proof. In the meantime, London remains Europe’s dominant financial centre, and the UK the leading destination for foreign direct investment overall.

“Stopping Brexit is more important than stopping Corbyn”

Finally, some City commentators have argued that stopping Brexit is more important than stopping Corbyn. In part this is because they wrongly believed that Boris Johnson would be unable to negotiate a new agreement with the EU to avoid ‘No Deal’. But it is mainly because they have been astonishingly complacent about the risks posed by a Labour Party bent on tearing up the rules of a liberal, free market economy.

We can all agree that the UK has an investment and productivity problem, and that more needs to be spent on public services. But Labour’s pitch is fatally weakened by the sheer scale of the amounts that Mr Corbyn is proposing to borrow and spend over a relatively short period of time. Any remaining fiscal credibility has surely been shredded by the last-minute decision to pay £58 billion to women affected by changes in the state pension age, regardless of need.

What’s more, even if Labour’s fiscal plans were sound, any good would be undone by the multiple attacks on private enterprise and property rights, and by further clumsy interventions in the setting of wages, prices and rents. Whatever you might think of Labour’s macro-economic policies, they would be undermined by a failure to grasp the importance of getting the micro-foundations right.

To be fair, the financial markets are waking up to these risks too. A Labour victory is now expected to cause sharp falls in asset prices and the pound, and raise interest rates. For once, I think the emerging consensus in the City is correct.

This piece was first published by the Daily Telegraph