So, it’s official. The global rating agency S&P has determined that the Russian government has defaulted on part of its international debt. In itself, this is not as big a deal as it may sound. Nonetheless, the unusual circumstances have revived concerns about the future of the US dollar as the reserve currency of choice for central banks around the world.

To recap, Russia is now judged to be in ‘selective default’, because it has attempted to repay holders of two US dollar-denominated bonds with Russian roubles. At the very least, this is a technical breach of the terms of the debt.

It will also probably lead to some material losses for bond holders, even though the Russian currency has partially recovered since its initial collapse after the invasion of Ukraine.

However, this default does not really matter, for three main reasons. First, it is no surprise. The financial markets had seen it coming and already priced it in.

Second, financial institutions have been reducing their exposure to Russia for a long time, especially after the illegal annexation of the Crimean Peninsula in 2014.

Third, Russia is not a big player in international bond markets anyway. Years of huge energy surpluses mean that Russian foreign debt is relatively small and is well covered by large reserves of foreign currency – provided Russia can access them.

This is where the wider angle comes in. The fact that Western sanctions have made it harder for Russia to service its debts has led some to question whether other countries might be quite as keen to hold so much of their international reserves in US dollar assets.

Of course, predictions of the dollar’s imminent demise as the world’s reserve currency of choice have been around for decades – and they have consistently been proved wrong.

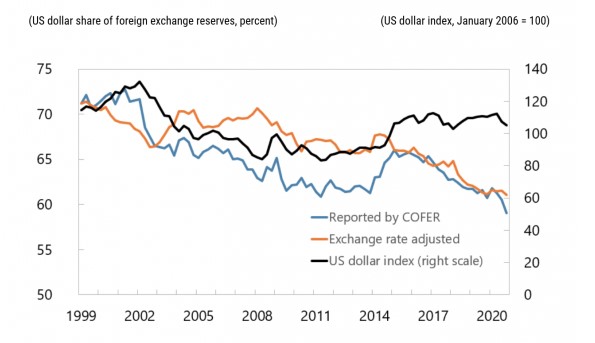

For most of the 1970s, 1980s and 1990s, about 65-70% of official reserves were held in US assets. This figure has since steadily declined – hitting a 25-year low in 2020 – but was still just under 60% at the end of last year.

Several factors could change the share of reserves held in any particular currency – including fluctuations in exchange rates (if the dollar rises or falls relative to other currencies, the share of total assets held in dollars mechanically rises or falls too), or fluctuations in the relative value of the underlying assets.

However, the main driver of the decline in the dollar’s share has been diversification by central banks, as shown by the ‘exchange rate adjusted’ line in the chart below. But it is also worth noting that the dollar itself has mostly kept its value against other major currencies, as shown by the US dollar index line.

What’s more, this is despite the relatively rapid growth of competing economies, notably China, and even the creation of a rival global currency, namely the euro.

This is because the fundamentals that made the US the reserve asset of choice have not really changed. The best way to think about this is to compare the dollar to the alternatives.

For example, the US has a strong institutional framework, operating under the rule of law, and with many Constitutional checks and balances. It is therefore a much more predictable and safe place to invest than, say, China, whose leaders can be much more capricious.

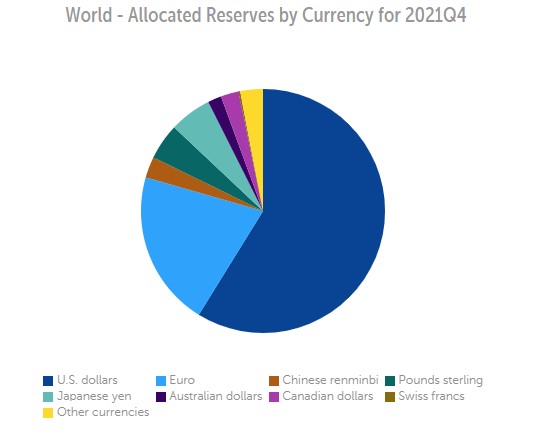

The US financial markets, including the government bond markets, are also relatively large and liquid. The same might be said of the euro area, but the euro has never really taken off as a reserve asset. The share of the euro in global reserves is still only around 20%, similar to where it was when the single currency was launched in 1999.

That might change if the EU ever morphed into a successful fiscal, banking and political union (obviously, a big if). But in the meantime, few investors see the euro as more than the sum of its parts, and especially the old Deutschmark.

China falls down on the pool of available assets too. There is an awful long way to go before the Chinese government bond market could rival the US.

In the meantime, the share of global reserves held in renminbi (2.8% in the final quarter of 2021) is still smaller than either the Japanese yen (5.6%) or, wait for it, the mighty British pound (4.8%). (The source for the chart and table below is the IMF COFER database, available here.)

Many countries around the world (notably in the Middle East and in Asia, including China itself) also still try to keep their own currencies stable against the US dollar, either with explicit pegs or some sort of managed arrangement. The de facto ‘dollar zone’ is therefore much bigger than the US economy itself.

You do not have to hold reserves in US dollars in order to defend a dollar peg. But the fact that so many economies are tied to the US dollar in some way reinforces its status as a reserve asset.

Finally, it is not obvious why the fallout from Russian sanctions should change this. It is possible that some dodgy regimes (perhaps China, or in the Middle East) might be less comfortable holding money in US assets. But then, what is the alternative?

The major developed countries are increasingly coordinating their policies, so moving reserves from the US to, say, the euro or sterling is unlikely to escape sanctions, or other regulatory controls. (I’m relatively upbeat on the prospects for the UK economy, but even I don’t see reserve diversification as a good reason to expect the dollar to weaken against the pound, or not to hedge currency risks.)

Keeping foreign currency reserves in renminbi assets might just swap one set of political risks for another, perhaps greater, and of course this is not an option for China itself.

China also faces another problem: the country is such a large holder of US assets (especially Treasury securities) that it would make huge losses if it become known that it was selling them.

In the long run, it does seem likely that the dollar’s share in global reserves will continue its gradual decline, with the euro and (increasingly) the renminbi as the main beneficiaries. However, this will happen at a glacial pace.

At most, countries like China might invest more of any new reserves, or the proceeds from maturing bonds, in non-US dollar assets. But they are unlikely to dump their existing holdings.

In the meantime, whether the actual market value of the dollar is higher or lower in five or ten years time against currencies like the pound will continue to depend on the usual drivers, including relative economic growth, inflation and interest rates. Even during global crises, the US dollar remains a safe haven.

In summary, I get why US-led sanctions against Russia have led some to question whether other governments might now be less keen on holding so many US dollar assets. But reserve asset diversification hasn’t had much impact on the value of the dollar so far, and I don’t expect that to change in the near future.

This is an extended version of a piece first published by the Spectator on 15th April 2022