In his Spring Statement speech the Chancellor made the eye-catching claim that ‘in the next financial year, we’re forecast to spend £83 billion on debt interest’.

This £83 billion figure was widely understood to be the amount that the government would actually pay out in interest in 2022-23. This has prompted lots of unfavourable comparisons with spending on other areas, such as defence. The reality, as usual, is more nuanced.

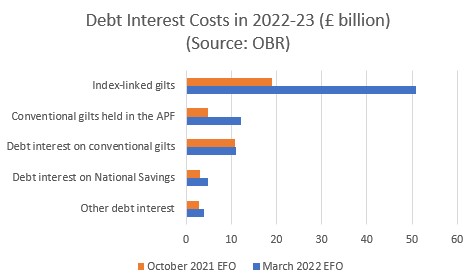

It may help to start by breaking down the £83 billion. My chart below summarises the main components of the forecast for 2022-23, and how it has changed in the last six months.

As you can see, the jump partly reflects an increase in the cost of conventional gilts held by the Bank of England’s Asset Purchase Facility (APF). These purchases are financed by issuing central bank reserves to commercial banks, which pay the Bank rate, and this has risen from 0.1% to 0.75%.

But the main factor behind the jump is a much bigger increase in the cost of inflation index-linked gilts. (See here for a detailed guide.)

These are bonds whose principal value (which is the amount investors get back at the end of the life of the bond) is linked to an official measure of inflation. In the UK this is the RPI, and the increase in the principal value is known as the ‘RPI uplift’.

These bonds also pay regular interest (a coupon) expressed as a percentage of the principal value of the bond. Because the index-linked element of these bonds is highly valued, these coupon payments can very low. Indeed, many UK index-linked bonds now pay a coupon of only 0.125%. (See here for a handy list.)

Here is an extremely simplified example (ignoring intra-year uprating and compounding). Suppose the UK government issued a 10-year index-linked bond with a face value of £100 and an annual coupon of 1%. If RPI inflation is 3%, at the end of the first year the principal value would increase to £103 and the first coupon payment (the amount paid out) would be £1.03 (1% of £103).

Suppose instead that RPI inflation is 10%. At the end of the first year the principal value would then be much higher, at £110, an increase of £7 compared to the scenario where inflation was only 3%. But the coupon payment would only be a little higher, at £1.10 compared to £1.03, an increase of just 7p.

This is a crucial point, because the bulk of the forecast increase in the debt interest in 2022-23 is accounted for by the RPI uplift to the principal value. The government will not actually have to pay this out until the bonds mature and are redeemed, which may not be many years, even decades, into the future. (The average maturity of UK inflation index-linked debt is more than 18 years.)

Does this matter? Some would say not. The additional government liability due to the jump in RPI inflation will indeed be incurred in 2022-23. Since the main measures of spending and borrowing are calculated on an accruals basis, rather than cash flow, it is therefore technically correct to say that the cost of debt is forecast to increase to £83 billion in the coming year.

It would also be irresponsible to suggest that we can forget about the additional costs, just because they won’t actually materialise until far into the future. (I’m not suggesting this!)

Nonetheless, the details here are important – for three reasons.

The first is political, or at least presentational. The Chancellor used the £83 billion figure as part of the justification for keeping £30 billion of headroom against his fiscal targets, rather than doing more now to ease the pressure on households and businesses.

The implication was that as we’re going to be spending a record £83 billion on debt interest in 2022-23, we can’t afford any more for tax cuts, or benefit increases.

But once you understand that this additional cost is mainly due to the RPI uplift (rather than a higher level of borrowing or debt), and that this cost will be spread over many years, the argument against immediate action is much weaker.

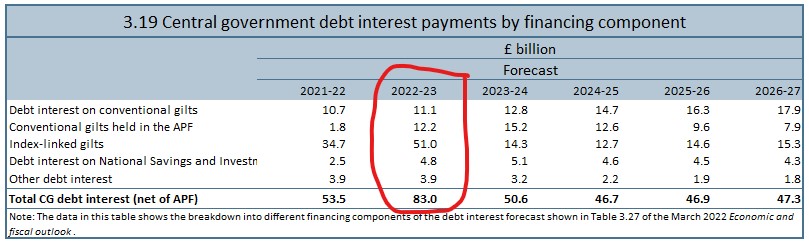

Even on the basis of the headline numbers, it is also worth noting that this jump in ‘debt interest’ is a one-off: ‘debt interest’ is forecast to peak at 3.3 per cent of GDP in 2022-23, but then to fall to 1.9 per cent in 2023-24 and to be back at its 2019-20 level of 1.6 per cent by 2026-27.

The table below (from the supplementary fiscal tables provided with the EFO) shows the corresponding figures in £ billions,

The second point is economic. Cash payments in the distant future are usually valued differently from payments that have to be made now, even if they are adjusted for changes in prices in the meantime. In other words, the ‘time value of money’ is not just about inflation. (If you think it is, ask yourself whether you would be happy with a real rate of return of zero on a long-term investment!).

For example, assuming at least some real growth in the economy, the burden of paying £83 billion in eighteen years time, even if uprated in line with inflation, should be less than the burden of paying £83 billion now. This is because £83 billion (plus RPI) will still represent a smaller percentage of national income.

Uncertainty plays a role here too. The amount of ‘debt interest’ that the government will actually end up paying will depend on inflation over the whole life of each index-linked bonds. If inflation is lower than expected, the cost to the government will fall.

In this case, it is uncertain whether the government will actually have to pay an additional £83 billion. Even if that is the correct figure for the additional liability in respect of inflation in 2022-23, it could be offset by lower inflation in future years.

Of course, the true figure might turn out to be higher. But here it is worth stressing that inflation can still be good for the public finances overall. Over time, the boost to tax revenues from higher nominal incomes and prices can more than offset the higher cost of servicing government debt. This is certainly what is happening now. The OBR has revised down its forecasts for borrowing in every year except 2022-23, and for the debt-to-GDP-ratio in every year.

The third point is financial. The RPI uplift will have relatively little impact on the government’s cash requirement (‘CGNCR ex’) in 2022-23, which is the amount that actually has to be raised from the markets to cover the gap between cash inflows and outflows.

Put another way, there will still be plenty of cash to spend on other areas, without having to issue loads more new debt.

So to answer my original question, is the government really about to spend £83 billion on debt interest in a single year? In purely accounting terms, and on an accruals basis, yes, and that’s all some might care about. But in my view, this figure gives a misleading picture of the economic, financial and policy implications of the jump in debt interest costs.