Who’d have thought the Treasury’s ‘Ways and Means’ facility at the Bank of England could cause so much excitement? The two parties have agreed a temporary extension of what is, in effect, the government’s overdraft account with the central bank. Cue great delight from advocates of printing money to pay for higher public spending, such as Positive Money, and equal displeasure from opponents. In reality, both reactions are overdone.

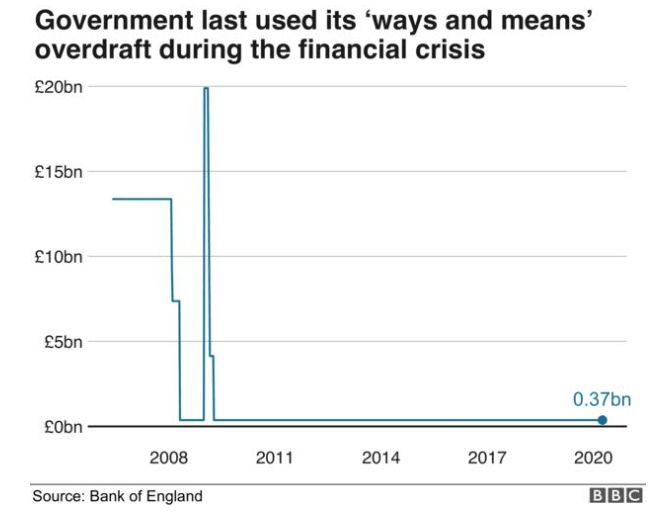

For a start, the ‘Ways and Means’ (W&M) facility is nothing new. Usually the outstanding balance on this account is around £370 million (peanuts in this context). But the government did make more use of it during the global financial crisis in 2008, when the balance hit its previous record high of just under £20 billion. The UK has therefore been here before, so a precedent has already been set.

What’s more, this is still only short-term borrowing that will have to be repaid (as was the case in 2008). Indeed, the plan is to do so ‘as soon as possible before the end of the year’. The announcement is therefore not necessarily the launch of ‘helicopter money’, in the usual sense of creating money to finance additional spending without any expectation of getting it back, or the permanent monetisation of debt. Nor is it some form of ‘Peoples QE’, or an endorsement of ‘Modern Monetary Theory’.

So, why is it necessary at all? Kudos here to the FT’s Economics Editor, Chris Giles, who astutely asked the new Bank of England Governor, Andrew Bailey, about the W&M facility back on 18th March. The Governor replied ‘it is one of the historical features we have had, it’s been there a long time and had a special status…I don’t think at the moment we’re seeing an inability of the government to fund itself. So, yes, it’s there but it’s not a frontline tool’.

If I may paraphrase his words, the Governor acknowledged that the greater use of the W&M facility is an option held in reserve, but that it was not yet needed. The question then becomes – what’s changed since 18th March?

The short answer is of course, ‘almost everything’, not least the start of the nationwide lockdown (on 23rd March). The Treasury has announced additional measures, notably the coronavirus Job Retention Scheme (20th March) to subsidise the pay of furloughed workers, and a similar scheme for the self-employed (26th March). In the meantime, there has been a surge in new claims for Universal Credit. All this will cost a lot of money – certainly tens of billions of pounds.

In principle, the government could finance all of this is in the usual way, by selling bonds (gilts) on the open market. Indeed, this will remain the primary source of financing. The stated intention is that all additional borrowing due to the coronavirus crisis will still be fully funded (eventually) through the normal debt management operations.

But in the short term, this primary source may not be sufficient, especially if there are sudden and unanticipated demands for a large amount of cash. (The Job Retention Scheme in particular looks set to cost a lot more than many first thought.) This is where the expanded overdraft facility comes in. It can be used to smooth the government’s cashflow and avoid the disruption that would be caused by frequent and erratic calls on the gilt and sterling money markets.

The announcement is therefore sensible and should be welcomed. Nonetheless, the move still has a broader significance. It does amount to ‘direct financing’ of government spending by the central bank, which is normally taboo.

To be clear, I don’t think it is fair to suggest that the Governor of the Bank of England misled the public by ruling out ‘direct financing’ in the past. The exchange with Chris Giles confirms that the greater use of the W&M facility was always on the table.

Nor do I think we should assume the Treasury put any undue pressure on the Bank. Presumably the Bank would also recognise that the government is now going to have to spend and borrow an awful lot more, and so the Treasury was pushing on an open door.

However, this still leaves plenty of room for doubt. If the temporary extension of the overdraft becomes permanent, then this would indeed be the monetisation of debt, with all the risks that would bring. If any government began to believe it could always force the central bank to print money to pay for higher spending, fiscal discipline would collapse, and too much money chasing too few goods would lead to a surge in inflation. This is of course a playbook we have seen in many other countries before.

For these reasons, I’m sure both the Bank of England and the Treasury would want the additional overdraft to be paid off by the end of the year. Given the strong demand for government bonds it should still be straightforward to wind down the facility and replace it with conventional borrowing in the gilt market. But I would certainly add any increased use of the W&M facility to the long list of emergency measures which should be unwound as soon as possible once the lockdown ends and normal economic activity can resume.

In the meantime, though, this is of course a gift to those who claim that the government can just shake the ‘magic money tree’ in Threadneedle Street for any of its pet projects. Most of us will not have heard of the ‘Ways and Means’ facility until today. From now on, we need to watch it like a hawk.