Here we go again… another day of alarming headlines about a tax ‘bombshell’ set to hit as soon as the Autumn Budget, with a ‘state pension grab’ chucked in too. Fortunately, there isn’t much substance in any of this – at least not yet.

Let’s start by contrasting what the Sunday newspapers are saying.

The Sunday Telegraph led with ‘bombshell tax hikes to pay for virus’. Apparently, Treasury officials are looking to find at least another £20 billion a year to plug a hole in the public finances left by the pandemic. Options include aligning capital gains tax (CGT) with income tax, cutting pension tax relief for higher earners, and a simplification of the inheritance tax system – all measures that would largely hit the better off. But others on the list include increases in fuel and other duties and the introduction of an online sales tax – which would hit practically everybody.

The Sunday Times went with ‘Sunak plans triple tax raid on the wealthy’. Interestingly, the sum mentioned was different (£30 billion), as were the options being considered. The Sunday Times focused on the possibility of hiking corporation tax from 19% to 24%, which might raise about half that target amount. The article also flagged up the possibility of aligning CGT and income tax, tackling pension tax relief, and a rethink of the triple-lock on the state pension (more on that below).

What to make of this? First, this is still largely speculation and most of it is actually not even new. The Treasury has been raising concerns for some time about the risk that long-term economic damage caused by the pandemic could leave a ‘structural deficit’ of tens of billions of pounds – and that this will have to be closed by tax increases or spending cuts.

Indeed, I remember the Daily Telegraph and Financial Times running similar stories – back in May – about the ‘stark options’ being considered to close this deficit. The choices then under discussion included increases in income tax and a two-year public sector pay freeze, neither of which seem remotely likely now.

The fact that the Sunday Times and the Sunday Telegraph each focus on different options suggests that the debate has not moved on much since then. I also suspect that the Telegraph is right to suggest that this is still coming from ‘Treasury officials’ and has not yet been adopted by the Chancellor himself (though obviously pinning this on Rishi Sunak makes for a better headline!).

Second, despite suggestions from both newspapers that tax hikes could begin as soon as the Autumn Budget, this is surely premature. In fact, I’m not aware of any serious economist who thinks that now would be a good time to be talking about raising taxes, let alone actually implementing any significant increases.

In part this is because the UK economy is only gradually emerging from an unprecedented recession. Consumer and business confidence are still fragile and both monetary and fiscal policy will have to support the recovery for the foreseeable future.

Bucking the global trend towards lower corporation tax (CT) rates would be particularly daft at a time when it is more important than ever to make the UK an attractive place for global businesses to invest. Even if a new (CT) rate of 24% would be close to the OECD average, it would still be a lot higher than it is now – and a big step in the wrong direction.

What’s more, it is far too early to say what the long-term impact of the pandemic on the public finances is going to be. It would be certainly be odd to raise taxes any time soon purely on the basis of a forecast for the public finances that could be very wrong.

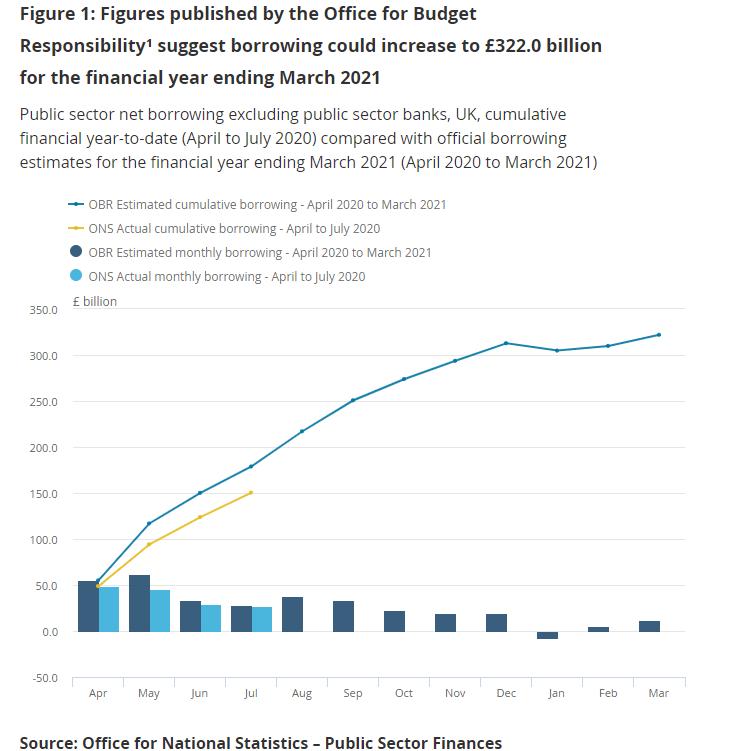

To illustrate this, government borrowing is currently running about £30 billion below the path projected by the OBR for this year! What confidence can we have that the Treasury has identified a £30 billion ‘black hole’ for many more years to come?

Above all, there is no urgency. The budget deficit should narrow sharply next year as the economy recovers and the emergency fiscal support can be withdrawn. The stock of debt will remain higher, but the burden of this debt as a share of national income will also start to come down. In the meantime, it should be readily financeable at historically low interest rates.

My gut feeling is therefore that the Autumn Budget will be another holding exercise. There might be some tinkering at the margin, targeted at the relatively wealthy. We had a taste of this in the March Budget which restricted the value of Entrepreneurs’ Relief (or Business Asset Disposal Relief as it is now known). I’d expect a similar measure or two this Autumn, perhaps raising a few billion from inheritance tax or pensions relief, but no game-changers.

The Chancellor will, however, have to do something about the triple-lock on state pensions – at least temporarily. But this is unlikely to be the ‘state pension grab’ that some seem to fear.

Recall that the triple-lock is a guarantee that the state pension will increase each year by the largest of 2.5%, consumer price inflation, or the annual growth in average weekly earnings. The problem is that average earnings are likely to surge next year as working hours return to normal, even if hourly pay rates are unchanged.

This is not something that was anticipated when the triple-lock was introduced, and suspending the link to average earnings for one year would be perfectly reasonable. It is certainly not obvious why anyone would expect state pensioners to receive what could be a double-digit percentage increase just because of this anomaly.

Instead, they could simply get the higher of 2.5% or CPI inflation – for one year only. Given the Manifesto commitment to keep the triple-lock, it would surely be politically impossible to scrap it completely this side of the next election.

In summary, I don’t think anyone – including Treasury officials – really thinks that now is the right time to start applying the brakes. There is an important debate to be had about the longer-term outlook for the public finances, especially given the demographic timebomb. However, the shells are unlikely to start falling soon.